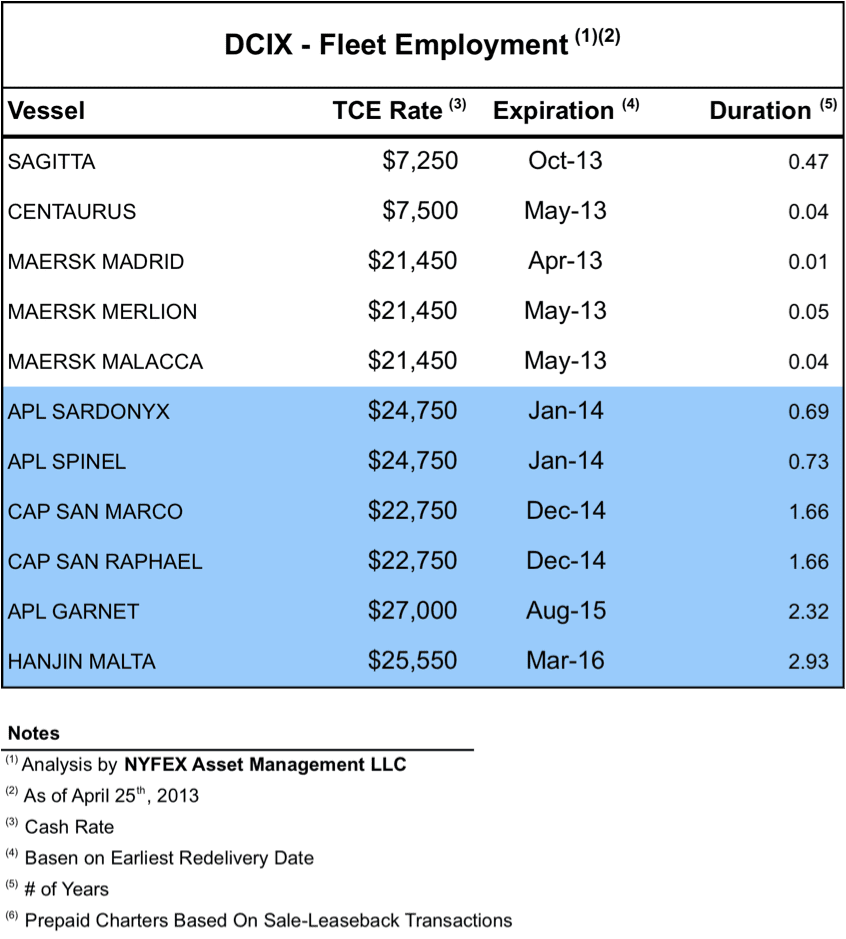

I recently had the opportunity to write an editorial on the sale of Maersk Madrid for demolition by Diana Containerships (DCIX). The disposal of the vessel represents a unique opportunity to analyze the return on investment for this particular asset. Since Maersk Madrid was part of a three vessel sale/lease-back deal between Diana & Maersk in April 2011, it also provides helpful clues regarding the profitability for the other two vessels (Maersk Merlion & Maersk Malacca), which are scheduled for redelivery to the company beginning in May of this year.

Maersk Madrid was delivered in June 2011, and commenced a two-year charter at a gross rate of $21,450 per day. Diana had purchased the vessel for $22.5 million, as part of a $70.5 million en-block deal for three panamax containerships. Following the delivery of the vessels, Diana had invested an additional $2.2 million to improve efficiency & safety onboard.

The acquisition of the Maersk vessels, which increased the company’s fleet at the time to five units, provided the critical mass and cash flow visibility for a successful IPO. In June 2011 Diana raised $121.5 million in net proceeds, by selling 16,916,667 shares at $7.50 per share.

click for larger

To lend support to the IPO, parent company Diana Shipping Inc. invested $20 million and members of Diana’s executive team separately purchased 1,625,000 shares. The IPO planted the seed for further expansion (after the demolition of Maersk Madrid the current fleet will number 10 vessels), including a subsequent $53.9 million equity offering last July.

It seems however that no good deed ever goes unpunished.

Less than two years after the company’s IPO, Diana Containerships finds itself in the awkward position of premature asset disposals. Weak freight markets and increased uncertainty regarding the long-term viability of panamax vessels in a post-panamax world, forced the company’s hand. This month, Diana decided to scrap the 24-year old vessel Maersk Madrid for $8.8 million.

In the table below I summarize the profit/loss and IRR analysis for Maersk Madrid. Taking into account daily operating expenses of $9,000 per day, and general & administrative expenses of $1,300 per day, the investment generated a negative IRR of 22%. On an undiscounted basis, Diana will be out of pocket approximately $7 million, a substantial loss considering the initial purchase price of $22.5 million.

Which begs the question: Will the other two vessels have a similar ending once they are redelivered from their lucrative charter deals? We will soon find out since both units have a redelivery window between May and August.

Bruised investors will learn some very helpful lessons.

First, charter rates based on a sale/lease-back deal are extremely hard to be replicated once their original term is up. Second, if timing is everything for a profitable investment in shipping, the window of opportunity on a second-hand asset purchase is much more narrow. Third, the cascade effect following the opening of the new Panama Canal in year 2014 will render older panamax vessels uneconomical.

Alas, nobody’s batting average is ever perfect. Diana Containerships has a very conservative capital structure with moderate debt outstanding, and is run by a competent management team that has skin in the game. Its current stock price already reflects lower asset valuations. I still like the company as an asset play. I don’t mind collecting a dividend either, but I understand that the current dividend payout is not sustainable.

Global container freight rates continued their upward climb this week as tightening capacity and strong seasonal demand pushed prices higher across the key east-west trade lanes. According to the latest Drewry...

A.P. Moller-Maersk has sharply upgraded its financial guidance for 2026, citing stronger-than-expected demand in the global container shipping market and a sustained rise in spot freight rates, particularly on trades...

South Carolina Ports (SC Ports) will temporarily suspend container operations at its Hugh K. Leatherman Terminal beginning August 1, marking the latest setback for the $1 billion facility that has struggled to gain momentum since opening just over five years ago.

June 29, 2026

Total Views: 2449

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 104,815 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 104,815 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club