By William Bennett,

(VesselsValues.com) – Both the BDI and the BCI have been hitting successive record lows. Capesize rates fell below $2000pd in January 2016 and with the current OPEX for a standard capsize sitting at around $6000pd, the majority of vessels are operating at a loss. Industry sources suggest that rates could sit somewhere between $6000pd and $8000pd for the remainder of 2016 but this is hardly a worthwhile improvement. Suggested period for recovery receives mixed estimates ranging from 12 months to five years with the majority suggesting 18-24 months.

Downturns in value have been less than satisfactory for current Capesize owners with some capes losing up to 60% of their value over the last 12 months. However, despite further expected downturns in value circa 10-15% according to broker sources, 2016 will be a good year for dry bulk acquisition; particularly cheap, high-risk capes.

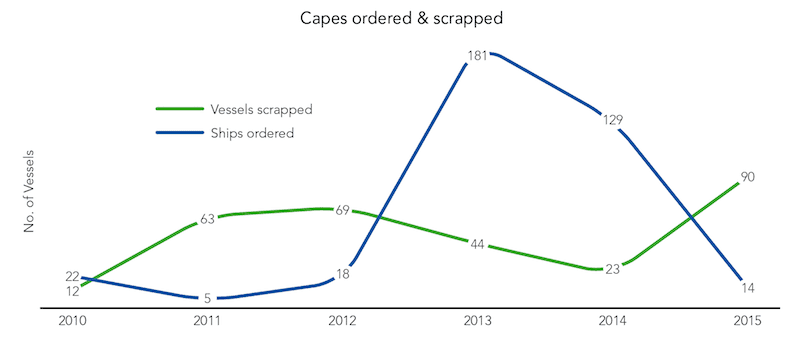

Fleet growth is of particular interest in the current climate. It is universally acknowledged that one of the root causes of the trough is tonnage oversupply. In 2015 Capesize new orders fell by 89% year-on-year. Only 2.8m deadweight tons were inked compared to 2014’s mammoth 26.8m. So fleet growth is slowing, however until issues of oversupply are directly addressed then a recovery is off the cards. Owners’ survival will be decided by their cost efficiency strategies, the age of their fleets and the depth of their wallets. Current talk spans between cold layup and scrapping.

It is estimated that cold layup will cost around $1500pd for a standard Capesize. If rates sit below $4500pd then this is the cheaper option. Rates are indeed currently below $4500 which is why cold layups over the coming months will doubtless become more commonplace.

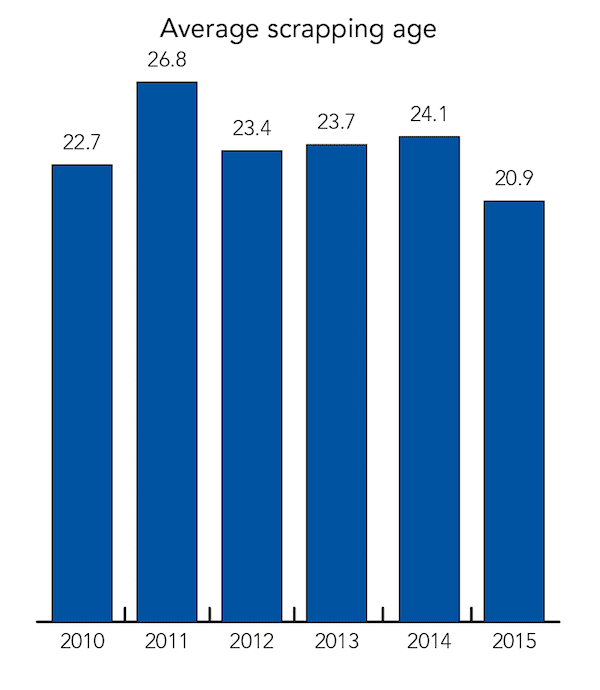

For younger vessels out of charter, layup is the lesser of two evils, the greater being demolition. In 2015 Capesize scrapping almost tripled on levels seen in 2014. A total of 15.1m DWT was sent for demolition. The average age of vessels being scrapped has fallen by around 25% – in 2015 it stood at 20.9 years compared to 2010 where the average vessel was 27.7 years old.

Much attention has recently been given to 15 year old ships, becoming a new ‘pivot’ age for demolition. No capes younger than 15 years have been scrapped to date, however three 15 years old capes were scrapped in 2015. There are approximately 140 Capesize vessels still live that are older than 20 years, while 257 are 15 years old or more. With some owners’ dwindling cash reserves and a glut of tonnage supply, younger scrapping may become the only option.

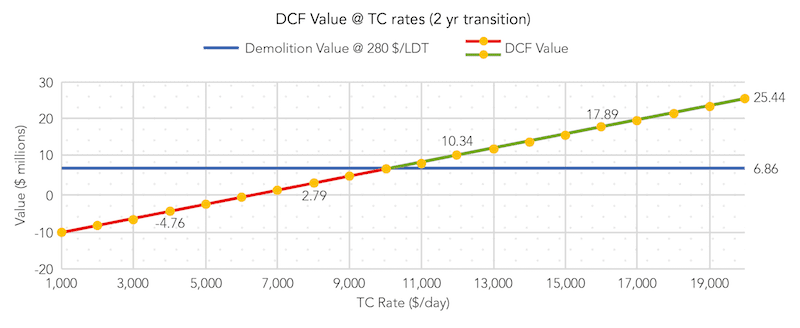

Scrapping, however, is going to be market driven as well as owner specific. The average scrap price actually increased by around 15% year on year despite heavy levels of recycling in 2015 (2015: 362 $/LDT compared with 2014: 316 $/LDT). At the time of writing, best subcontinent rates are approximately 280 $/LDT making a Cape of 22,500 LDT worth around $6.4m. Using the VesselsValue Discounted Cash Flow (DCF) module to compare the scrap value against the long-term earnings value of a 15 year old cape reveals some stark facts. In order to achieve a DCF value equal to the demo value, long-term rates with a 2-year recovery horizon would have to sit at $10,900pd. Below $8,000pd DCF value starts to run into the negative suggesting that too meagre a recovery will drive owners into the dirt.

A generic 2001-built Capesize (15 years old) assumed high quality yard and 170,000 DWT has a current market value of approximately $6.6m. This is alarmingly close to the $6.4m quoted above for demo. On the 14th January the 172,500 DWT Koryu 2000 blt, NKK, sold for USD 6m, demonstrating what current conditions are like. Some investors see the investment opportunity, particularly in ‘upcycling’ as dry bulk become obsolete. Not too long after the Koryu, the Nisshin Trader (172,500 DWT, 2001 blt, Universal) sold for USD 6.25m for conversion into a mobile power station by Karadeniz shipping based in Istanbul. It is unknown whether the new Chinese owners of the Koryu will continue to trade the vessel but no trading buyers were found for the Nisshin Trader providing further argument for scrap or more creative options.

The sector has also seen exits and partial exits of large market players. With the Nord Energy, Norden make their exit from the Capesize sector planning to focus further on their Panamax and Supramax portfolios. The deal occurred in unusual circumstances following a swap for Bocimar’s Supramax, the CMB Maxime. Star Bulk also seem to be beating a hasty retreat having offloaded 8 Capes since December 2015 for a net $295.3m. Current market activity shows clearly that the next 2 years will deliver a whole host of death-defying survival strategies and perhaps some of the weird and wonderful too.

Willial Bennett is a Valuation Analyst at VesselsValue.com, an online ship search, valuation and mapping service for Bulkers, Containerships, LNG, LPG, Tankers.

Editorial Standards · Corrections · About gCaptain

Join The Club

Join The Club