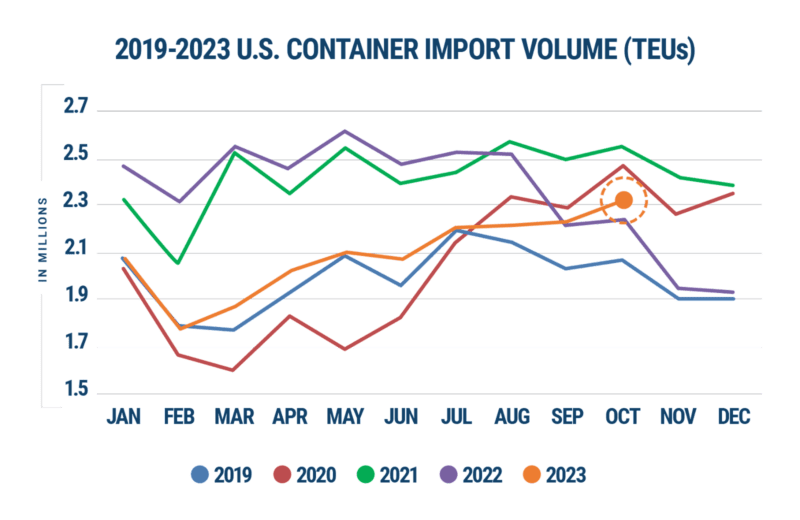

U.S. container import volume saw a significant increase in October 2023 compared to September and has even surpassed the levels seen in October 2019 before the pandemic, according to the latest report by Descartes Systems Group.

The November Global Shipping Report shows U.S. container import volumes in October 2023 rose by 4.7% from September, reaching 2,307,918 twenty-foot equivalent units (TEUs). This marked a somewhat surprising 3.9% increase compared to last October, and a substantial 11.4% jump from pre-pandemic levels in October 2019.

Contrary to the usual pre-pandemic peak season decline that typically begins in August, import volumes have continued to rise and have approached the levels that caused port congestion during the pandemic, according to Descartes.

Chart courtesy Descartes

Imports from China increased by 2.3% in October 2023 compared to September, reaching 886,842 TEUs. However, this is still a decrease of 11.6% from the peak in August 2022. China accounted for 38.4% of total U.S. container imports in October, a decrease of 0.9% from September and 3.1% from February 2022.

Despite favorable labor conditions and concerns about the Panama Canal drought, the top West Coast ports continued to lose market share of imports. The top five East and Gulf Coast ports accounted for 45.1% of the total import container volume in October, marking a 3.0% increase. On the other hand, the top five West Coast ports saw their market share decrease to 39.6%, which was down by 3.7%.

Despite increased import volume, port transit times improved or remained stable, reaching some of their lowest levels. Most top ports saw delays decrease in October, with the Port of Seattle experiencing the greatest improvement of 1.6 days. The Port of New York/New Jersey, however, saw a slight increase of 0.1 days compared to September.

“October has traditionally been a stronger month than September. However, the last two months show an increase above pre-pandemic 2019 import levels, which are counter to the declines expected at the end of the year,” said Chris Jones, EVP Industry at Descartes. “The drought in Panama still does not appear to be affecting Gulf Coast port volumes or to have caused a shift to West Coast ports.”

By Brendan Murray Jun 6, 2026 (Bloomberg) —Container shipping rates jumped over the past week amid higher fuel costs, congestion at some Asian ports and a pickup in demand heading into...

Container freight rates are rising sharply across major east-west trades as the conflict in the Middle East, disruption at key Asian transshipment hubs, and growing fears of an energy crisis...

CMA CGM has reported “resilient” first-quarter 2026 results as the world’s third-largest container carrier navigated ongoing disruption tied to the Middle East crisis, volatile freight markets, and shifting global trade flows....

May 26, 2026

Total Views: 930

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 105,296 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 105,296 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club