An ship carrying LNG from the U.S. East Coast to Japan transits the Expanded Panama Canal. Photo taken in April 2018. Photo: Panama Canal Authority

By Clyde Russell (Reuters) – Spot liquefied natural gas (LNG) prices in Asia have roared back to life in recent weeks, boosted by temporary and longer-lasting factors and recovering from being one of the commodities hardest hit by the coronavirus pandemic.

Spot cargoes for delivery in November to northeast Asia LNG-AS were assessed at $5.50 per million British thermal units (mmBtu) in the week ended Oct. 9, the highest price this year and a sixth consecutive weekly gain.

That nearly triples a record low of $1.85 per mmBtu, hit in separate weeks in May when many of Asia’s economies were locked down to combat the spread of the coronavirus.

Among the factors now driving spot LNG prices higher is the expectation of stronger demand over the northern winter, as colder temperatures are forecast due to the likely emergence of a La Nina weather phenomenon.

Japan’s meteorology bureau said on Oct. 9 there is a 90% chance this winter of a La Nina, an event in which colder ocean temperatures in the equatorial Pacific result in colder weather in North Asia and higher rainfall across the region and down to Australia.

The forecast for a La Nina is helping drive spot LNG prices for winter, with December delivery cargoes at $5.70 per mmBtu, a 20-cent premium to those for November.

It’s worth noting that spot LNG prices are typically seasonal, reaching their peak during the northern winter and hitting lows during the low-demand shoulder seasons between winter and summer.

Last winter, spot LNG’s high was $6.80 per mmBtu, reached in mid-October – early compared to prior years – but showing that the current price may have room to rally.

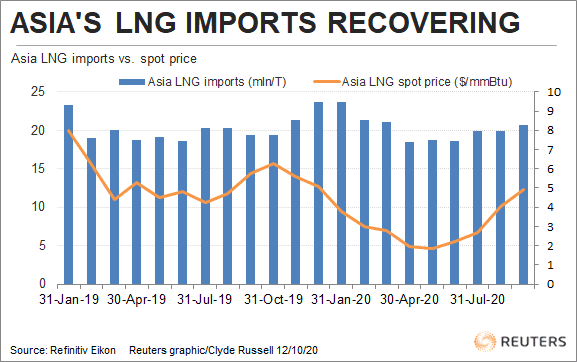

There is also evidence LNG flows to Asia are rising. Refinitiv vessel-tracking and port data show 20.68 million tonnes of the super-chilled fuel was discharged in the region in September, up from 19.86 million tonnes in August and 19.44 million in September 2019.

Japan, the world’s top importer, saw September arrivals of 6.4 million tonnes, up from 6.26 million in August and above 6.35 million in September last year.

Second-biggest importer China had imports of 5.42 million tonnes in September, down from August’s 5.88 million, but well above the 4.72 million in September 2019. China’s August imports were the highest since January.

South Korea, third-largest, had imports of 2.64 million tonnes in September, up from August’s 2.09 million, but slightly below last September’s 2.73 million.

No. 4 India took 2.1 million tonnes in September, down slightly from August’s 2.25 million, but up from 1.93 million in September last year.

U.S. BOOST

Rising U.S. natural gas prices, more likely a temporary factor, are also driving spot prices higher in Asia. Henry Hub futures hit their highest intraday mark on Monday since January 2019.

The gas futures contract touched $2.955 per mmBtu in early Asian trade, more than doubling the low for the year so far at $1.432 on June 26.

Hurricane Delta, which hit the U.S. Gulf Coast over the weekend, led to natural gas wells being shut, cutting U.S. output to its lowest in 26 months. Several U.S. LNG producers also had to shut down or curtail production because of the storm.

While production will recover after the hurricane, it is possible that U.S. natural gas prices remain at higher levels as winter demand approaches.

This would give Asian spot LNG prices something of a floor since they have tended to fall when U.S. producers are able to access cheap feedstock and undercut other major exporters, such as Australia and Qatar.

There are also supportive supply-side issues benefiting spot prices and relieving some of the pressure from the overall global LNG market’s current state of structural oversupply.

Chevron is undertaking a phased shutdown of its 16.5 million tonnes-a-year Gorgon project in Western Australia state, while Royal Dutch Shell is still working to bring its troubled 3.6 million tonnes-a-year Prelude floating LNG venture back into production.

Overall, spot Asian LNG has gone from being in the doghouse of global commodities to being a star performer, with the main risk to the rally being if the anticipated colder-than-usual weather fails to materialise this winter. (Editing by Tom Hogue)

Editorial Standards · Corrections · About gCaptain

This article contains reporting from Reuters, published under license.

Join The Club

Join The Club