Pangea LNG announced today that they have been granted a long-term, multi-contract authorization by the U.S. Department of Energy (DOE) to export liquefied natural gas (LNG) to free trade agreement (FTA) nations from its South Texas LNG Project currently in development on Corpus Christi Bay.

FTA countries covered by the DOE authorization include Republic of Korea, Australia, Bahrain, Canada, Chile, Colombia, Dominican Republic, El Salvador, Guatemala, Honduras, Jordan, Mexico, Morocco, Nicaragua, Oman, Panama, Peru and Singapore.

In December, Pangea LNG filed an authorization request with the DOE to export LNG to any country with which the U.S. does not have a free trade agreement. That application is still pending.

“Approval by the US DOE is a positive step forward for this project, which represents a significant investment in the development of the LNG market in the U.S.,” said John Godbold, Pangea LNG project director.

More information about this project can be read HERE

Pangea LNG will be authorized to export up to 8 million metric tons per annum (mtpa) of LNG produced from domestic gas fields for a 25-year term commencing on the date of its first export. That amount is equal to 1.09 Bcf/day of natural gas.

Putting this project in some perspective

In a recent study conducted by Deloitte MarketPoint, which assumed total US LNG exports of 6 Bcf per day, they predicted “a weighted-average price impact of $0.12/MMBtu on U.S. prices from 2016 to 2035 as a result of the 6 Bcfd of LNG exports.”

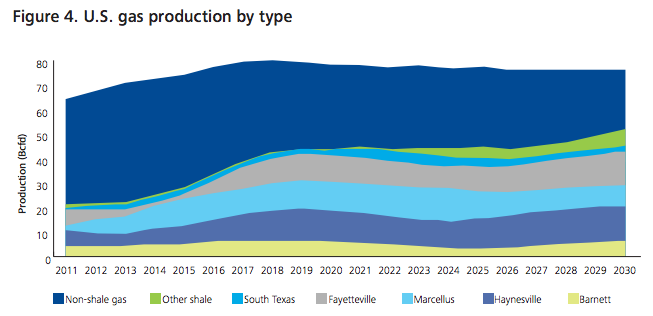

Chart courtesy Deloitte MarketPoint

The above chart represents natural gas production in the United States out to 2030. Note the flatness of the production rates. In their report, Deloitte notes that, “many upstream gas industry observers today believe that there is a very large quantity of gas available to be produced in the shale regions of North America at a more or less constant price. This would imply that they also believe that natural gas supply is highly “elastic,” i.e., the supply curve is very flat.

The Reference Case, according to Deloitte, “projects shale gas production, particularly in the Marcellus Shale in Appalachia and the Haynesville Shale in Texas and Louisiana, to grow and eventually become the largest component of domestic gas supply. Increasing U.S. shale gas output bolsters total domestic gas production, which grows from about 64 Bcfd in 2011 to almost 80 Bcfd in 2018 before tapering off.”

Any chance the production numbers are exaggerated?

Considering the top energy firms in the world have poured billions into this sector, it’s unlikely. Here are some numbers via Deloitte’s report:

ExxonMobil paid $34.9 billion to acquire XTO, which specialized in shale gas development, and later purchased two small shale gas exploration companies (Bloomberg, June 9, 2011).

Chevron acquired Atlas Energy Inc. and its 622,000 acres in the Marcellus Shale for $3.58 billion and subsequently purchased additional acreage from smaller operators (Bloomberg, May 4, 2011).

Shell acquired East Resources for $4.7 billion to double its reserves of shale gas (Bloomberg, May 28, 2010).

Statoil signed deals with Chesapeake and Talisman for shares in jointed development of shale gas plays with these companies (Reuters, October 10, 2010).

Qatar appears to have loaded its first liquefied natural gas cargo after the widening conflict in the Middle East forced it to halt fuel production and declare an unprecedented force majeure to buyers.

Danaos reported solid fourth-quarter earnings for 2025 while locking in $4.3 billion in contracted revenue and expanding into LNG through a new partnership tied to the Alaska LNG project. Strong charter coverage and high fleet utilization continue to anchor earnings visibility through 2028.

European buyers are aggressively importing liquefied natural gas from Russia’s Arctic Yamal LNG project as the continent prepares for a full EU ban on Russian LNG from January 2027, new figures compiled by advocacy group urgewald from Kpler data show.

February 4, 2026

Total Views: 3118

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 105,171 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 105,171 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club