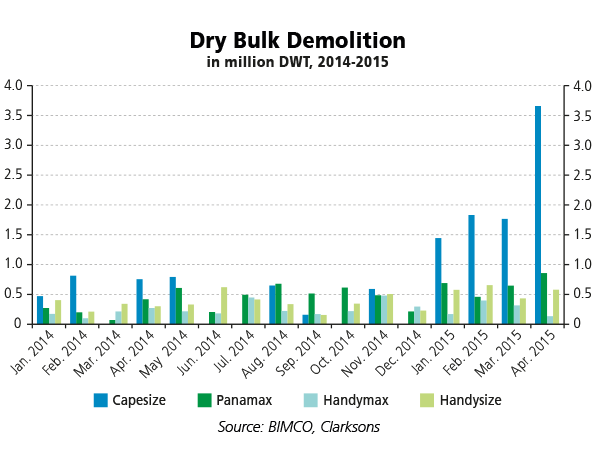

[contextly_sidebar id=”blTEeOrrbM06h22rx3534xyHBlK76W9e”]The Capesize dry bulk demolition market is off to its busiest start ever in 2015 amid some of the lowest dry bulk freight rates in the last three decades.

According to the world’s largest shipowner association BIMCO, during the first four months of 2015 a total of 52 Capesizes with a total DWT of around 8.7 million have been sold for demolition. Bimco points out that with those numbers the market is well on its way to break the 2012 record where a total of 70 Capesize ships were scrapped.

Chief Shipping Analyst at BIMCO, Peter Sand, Says: “The high amount of Capesize demolition will benefit the segment. Although increasing scrapping was expected the actual development exceeded BIMCOs expectations. This could have a positive impact on the market.”

The demolition of Panamax ships has also been on the rise in 2015 and although the development is not quite on par with the Capesizes it is still substantial, Bimco notes. In 2015 as much as 2.6 million DWT has already been sold for demolition equaling more than half of last year’s total where 4.8 million DWT were scrapped.

For Handymax and Handysize demolition has also increased in 2015. For Handymax just over 1 million DWT of tonnage has been scrapped so far in 2015, 34 % more than the same period last year, according to Bimco. For Handysize the numbers are 2.2 million DWT so far, up 79% from last year, Bimco says.

The dry bulk market has long suffered from weak freight rates stemming from falling demand and an oversupply of ships, so the increased demolition of capesizes in particular comes at much needed time for the market.

Credit: BIMCO

But it’s not all good news.

Bimco notes that despite worsening freight market conditions, the demolition of dry bulk tonnage has not been adapting fully to this trend as could be expected, at least until now. During 2014 bulk carriers equaling 16 million dead weight tons (DWT) were sold for demolition, down from more than 23 million DWT in 2013, according to Bimco.

Bimco also points out that scrap prices are under pressure from a general diminishing demand for steel in addition to cheap steel coming out of China. With low scrap prices, currently around USD 370 per light displacement ton (LDT) owners are more reluctant to let go of their ships despite being pressured from poor freight market conditions.

However, data from the first four months of 2015 shows that more owners are scrapping their ships than ever before.

Longer average sailing distances are expected to support dry bulk demand through 2026, helping offset rising fleet growth and keeping market conditions relatively stable before weakening in 2027, according to...

Cargill has taken delivery of its first green-methanol dual-fuel dry bulk vessel, a milestone in the agricultural giant’s push to cut emissions and test alternative fuels in day-to-day shipping. The Brave...

Seaborne coal shipments to China fell 10% in 2025 as increased domestic supply and weakening demand from steel manufacturing and electricity generation combined to reduce the world’s largest coal importer’s...

January 14, 2026

Total Views: 642

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 107,412 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 107,412 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club