For the world’s largest crude oil tanker company, 2013 was another year of losses. Frontline Tankers reported today their third yearly net loss in a row with negative results of $188.5 million. This figure is more than double the loss recorded in 2012 of $82.8 million and in 2011, the company recorded a loss of $529.6 million.

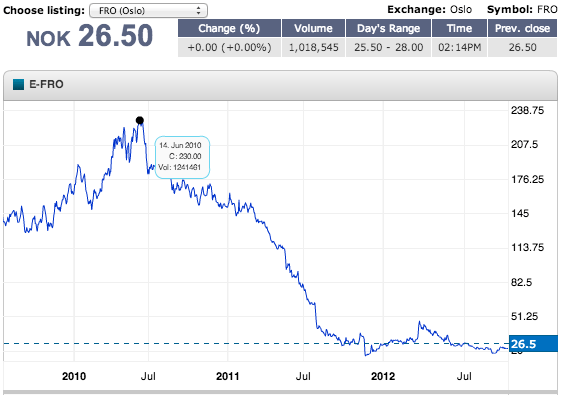

2010 was the last time the company was profitable, but oddly enough, the company’s share price has more than doubled since November 2013 reaching NOK 26.5 on the Oslo stock exchange. Although this price not been seen since July 2012, this pales in comparison to mid-2010 highs above NOK 200.

via Frontline

Frontline reports average daily time charter equivalents (TCEs) earned in the spot and period market in the fourth quarter by

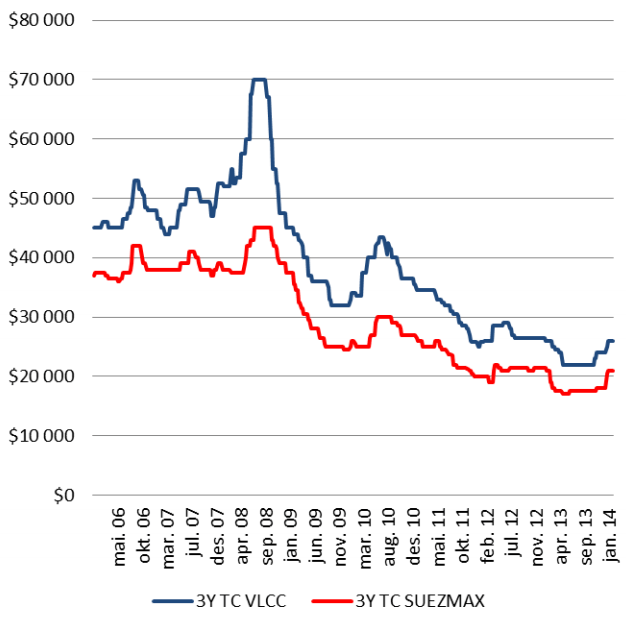

the Company’s VLCCs and Suezmax tankers were $22,400 and $12,900, respectively. These rates are still at historic lows for the crude tanker market as the following graphic shows.

Source: Clarksons

Frontline notes that the supply/demand balance looking ahead is a very fine balance, “can easily be changed by increased fleet supply caused by increased ballast speed, decrease in vessel scrapping and aggressive newbuilding ordering.”

In the company’s earnings call, CEO Jens Martin Jensen highlights this fine balance noting that an increase of vessel speed by 2 knots would equate to a virtual fleet increase of 10 percent. In addition, he notes that even with late 2013 improvements in the VLCC and Suezmax segments, the current slow-down in the LNG market as well as somewhat slower movement in the offshore sector could result in yard capacity opening up at Asian yards. This situation may result in an increase in orders for large crude tanker newbuilds.

Current newbuilding prices for VLCCs and Suezmax vessels are around $97 million and $67 million, respectively.

Frontline notes they have $1,058 million in debt obligations, and they note that the full repayment of that debt hinges “on a sustained improvement in tanker rates in the years to come.”

Frontline plc, one of the world’s largest publicly traded operators of crude oil tankers, reported its strongest adjusted quarterly earnings in more than 20 years on Friday, as the disruption of...

President Donald Trump said Tuesday he has directed the U.S. government to provide political risk insurance and financial guarantees for maritime trade transiting the Persian Gulf, while signaling that U.S....

A shipowner’s once-in-a-generation wager on oil tankers has made it so powerful that it controls an overwhelming majority of supertankers that can collect American oil next month.

February 26, 2026

Total Views: 1824

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 104,432 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 104,432 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club