Scaling up the availability of low and zero-emission fuels will be challenging. While the long term destination is clear, in the medium term the industry will need to confront the reality of scarce green resources, says COO of SEA-LNG, Steve Esau.

Steve Esau, COO at SEA-LNG,

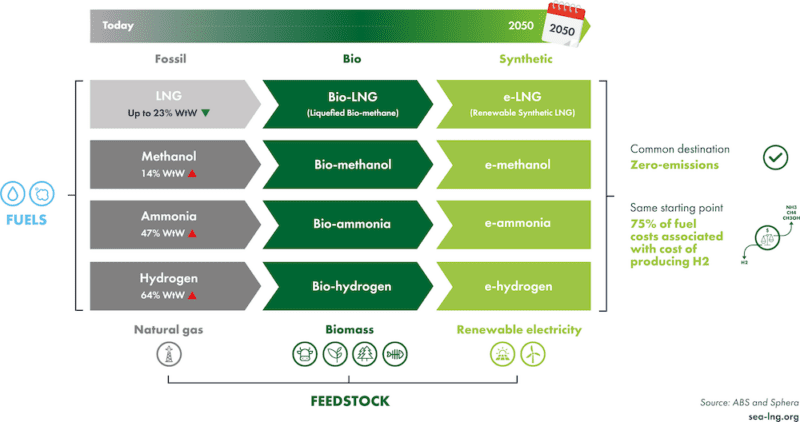

The benefits of alternative maritime fuels are a current topic that is not always fully explained. For LNG, we understand that there is a reduction in carbon of up to 23% in the two stroke engines which dominate the installed base. Adding increasingly available bio-LNG products produced from waste as a drop-in fuel and implementing fuel saving measures can reduce greenhouse gas emissions to meet IMO targets in the medium term. Longer term, as the hydrogen economy driven by renewable energy develops, synthetic LNG (e-LNG) can continue the journey to net zero.

Let’s take a look at the main low and zero emission marine fuel candidates that are being discussed today. In any analysis of alternative marine fuels it is important to emphasise that all share the same generic pathway to decarbonisation. This pathway moves from fossil-fuels today to an electro-fuel (e-fuel) destination. While much discussion focuses on the end goal, far less consideration is given to how to get there from where we are today. Before the vast quantities of renewable hydrogen which will be necessary for the production of e-fuels become available at low cost, the shipping industry will likely need to use biofuels or biogases derived from sustainable biomass – that is biomass that does not compete with food, fodder or fibre. These resources are scarce, and their use in maritime will face competition from other sectors, especially aviation.

Apple-to-Apples

Recognising the shared decarbonisation pathway, when we discuss alternative marine fuels, we should do so on an apples-to-apples basis. This means we should be careful to properly identify the fuel – highlighting whether a fuel is grey or green, and whether a green fuel is biogenic or an electro-fuel. The different fuel families have significantly different emissions profiles, availability and costs.

Almost all methanol, ammonia and hydrogen available today is grey, not green. Grey methanol increases greenhouse gas (GHG) emissions by 14% on a full lifecycle, well-to-wake (W-t-W) basis compared to VLSFO due to the large amounts of fossil energy required to produce it. This moves the shipping industry away from decarbonisation. Grey ammonia is even worse, with a W-t-W GHG performance almost 50% worse than VLSFO. By contrast, grey LNG offers an immediate reduction in GHG emissions of up to 23%, including methane slip, for the two stroke engines which move most of the world’s shipping tonnage. For the methanol and ammonia pathways, this means large volumes of scarce and expensive green fuels will be needed to achieve emissions reductions comparable to those available from fossil LNG. For example, for methanol a 30% green blend will be required to achieve parity with grey LNG.

Green fuel supply

This leads us on to the topics of fuel availability and the best use of scarce resources. Methanol and LNG are the alternative fuels currently dominating the new build order book, and so are in focus here. The recent flurry of orders for methanol dual-fuel vessels in the container sector has prompted the question: What fuel are these vessels actually going to use?

Methanol demand from shipping will amount to almost 14 Mtpa by 2028. To reduce GHG emissions, the methanol fleet will need to use green methanol, however global green methanol production (almost all bio-methanol) is currently 0.75 million tonnes per annum (Mtpa); this represents about 6% of the energy consumption of the methanol-fueled vessels in operation and on order. There is clearly a massive scaling challenge, exacerbated by the fact that large amounts of green methanol are required to simply achieve emissions parity with VLSFO, let alone LNG. The Methanol Institute estimates a potential green methanol production of about 8 Mtpa by 2028. The question is: how much of this fuel will make its way to shipping when it is needed by the chemicals industry where there are no obvious substitutes?

Bio-LNG (liquified biomethane) production is already well-established. Global biomethane production currently amounts to 30 Mtpa if converted to bio-LNG, which represents approximately 90% of the total energy consumption of the LNG-fueled fleet. Longer term, the International Energy Agency (IEA) estimates a global biomethane production potential of 600 Mtpa in bio-LNG terms.

Infrastructure

Availability is not just about supply but also about infrastructure. Methanol is a niche market mainly serving the chemicals industry. Annual production is a small fraction (10%) of the LNG market and the associated global infrastructure is less developed as most methanol (65%) is produced and consumed locally. Although methanol storage infrastructure exists in a number of ports, these facilities are generally small and there are currently no methanol bunkering vessels in operation and only seven on order. LNG bunkering leverages the large-scale infrastructure provided by a global network of 270 LNG liquefaction and regasification terminals and is available in 185 ports worldwide. There is a global LNG bunkering fleet numbering 50 vessels with a further 23 on order. As for bio-LNG, it is already commercially available in approximately 70 ports, mainly in Europe and North America.

Scarce resources

In the medium term, shipping is going to be dependent on biofuels and biogases for decarbonisation as they are much cheaper and more widely available than electro-fuels. However, they represent a relatively scarce resource which needs to be used carefully and directed towards the hardest sectors to decarbonise such as shipping, aviation and HGV road transportation.

Plans for green methanol production announced to date for shipping are dominated by projects in which bio-methanol is produced from bio-methane. This means a scarce green resource, bio-methane, which can already be used as a fuel, bio-LNG, is being used as a feedstock. This process is about 65% efficient, compared with 95% efficiency obtained in liquefying the same bio-methane into bio-LNG. As a result, significant quantities of precious green energy will be consumed to make a more expensive fuel, bio-methanol – a fuel which you will need in greater quantities to achieve emissions parity with LNG. This does not seem to make sense, environmentally, or commercially.

Consequences

Given this lack of green methanol availability compared with demand, and the fact that grey methanol increases, rather than decreases GHG emissions, there is a major risk that ship operators will run their methanol fleet on VLSFO for many years while they wait for supplies of the green fuel to become available at scale. This is likely to result in significant delays to decarbonisation and a large number of vessels that will not be compliant with IMO and EU emissions targets and associated regulations. The same challenge is likely to exist for the ammonia and hydrogen pathways. Here, the medium term dependency is on the availability of carbon capture and storage infrastructure to produce blue fuels – a nascent industry with another significant scaling risk.

The bottom line is that we must pay more attention to the implications of the different decarbonisation pathways, both environmental and economic. We must also recognise the issue of scarcity, while working on a common challenge: ensuring there are adequate supplies of renewable hydrogen for electro-fuel production and associated transportation, storage and bunkering infrastructure in the long term. With LNG, the decarbonisation process starts today and provides a low-risk, incremental pathway to net zero emissions making best use of limited green resources.

Steve Esau is COO at SEA-LNG, a multi-sector industry coalition established to demonstrate LNG’S bene?ts as a viable marine fuel.

ABS has awarded Approval in Principle (AIP) for a concept design for a nuclear-powered 15,000 TEU containership developed in collaboration with the Korea Research Institute of Ships and Ocean Engineering...

SEA-LNG says liquefied natural gas continues to dominate orders for alternatively fueled ships, while biomethane production and bunkering infrastructure are expanding as the shipping industry searches for practical pathways to...

Alternative-fuelled vessel orders eased during the first half of 2026, but LNG continued to dominate newbuild activity as shipowners favored proven fuel technologies while keeping an eye on emerging alternatives....

July 2, 2026

Total Views: 395

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 104,535 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 104,535 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club