Regardless of the state of the global economy, the world renowned Fifth Avenue in New York City is always bustling with optimistic shoppers looking for some relief through retail therapy. It appears that tanker owners, despite the market’s ongoing doldrums, have taken the same approach as they have certainly flexed their checkbooks at shipyards this year.

Just take a look at the 2013 orderbook.

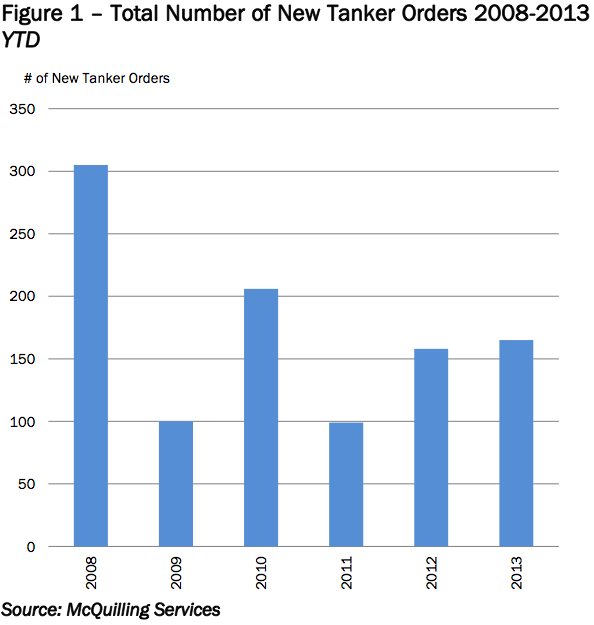

Between January and July there have been 165 orders placed for tankers 27,500 dwt and above. This is already in excess of the total orderbook recorded in 2012 which was 158 vessels. At present, it appears that 2013 figures are unlikely to reach the robust levels of 2008, but 2010’s figure could be possible (Figure 1). This activity has been somewhat surprising, given the previous year’s high orders.

Some of this ordering activity can also be attributed to asset values remaining low or continuing to fall this year, presenting an opportunity to buyers with deep pockets or access to financing. Despite the majority of activity occurring in the smaller sized tankers, some market participants recognize the value in the larger tankers as well.

The VLCC sector has been recording an upward trend in orders. Most of the orders have stemmed from players in the Far East. There were 14 orders in 2011 and 13 in 2012 with year-to-date activity in 2013 at 16 thus far. However, it appears unlikely that all of the VLCC orders will exit yards, given the status of some owners and yards.

Suezmax ordering has been limited, with only a total of 4 orders thus far in 2013 compared to 2011 and 2012 when the orders totaled 22 and 30, respectively (Figure 2). However, given the surplus of Suezmax tonnage and their increasing competition with VLCCs, these lower orders are critical for future fleet fundamentals. Between the years 2009-2012, there was a net fleet growth of 115 Suezmax vessels as compared to only 39 between the years 2001- 2008. Given these relatively strong numbers, concerns regarding tonnage surplus is likely to remain. Further pressure to demand has surfaced from rising US oil production, which is reducing demand for West African imports.

Aframax/LR2 sized vessel orders are also on the rise after two years of relatively low contracting. In 2013, orders have started to rebound with a total of 34 orders year-to-date, which could knock the projected balanced fleet growth offline. Support for these sectors also stems from port accessibility and the potential of these vessels to dirty or clean up, if a coating is added. Additionally, the US oil boom has provided some support for Jones Act tanker ordering. Panamax and LR1 orders have continued to be limited due to the fleet’s trade marginalization and there has only been one order in 2013.

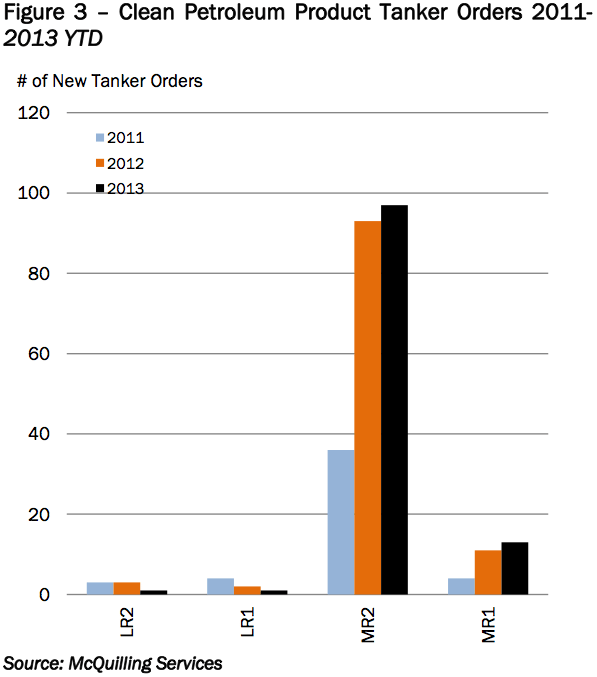

The sector that continues to dominate the available yard slots in recent years are MR2s. Between 2011 and 2012, orders have ballooned from 36 to 93 (Figure 3). The pace has continued in 2013 and orders have thus far tallied 97. In terms of ordering activity, two companies have dominated the landscape, Sinokor and Scorpio Tankers.

Our proprietary data shows that in 2011 and 2012 net fleet growth in the MR2 sector was 30 vessels, whereas the 2013 forecast anticipates that the fleet will expand by 40 vessels, highlighting the positive sentiment surrounding the tanker class. MR1s are showing a similar trend to MR2s, but on a much less dramatic level. Orders for MR1s in 2013 are at 13, already surpassing the previous two years’ total. Like the MR2 sector, orders have been dominated by a relatively narrow customer base.

The robust ordering activity in 2013 has been fueled by low asset rates and owners with healthy balance sheets having the opportunity to snatch bargain basement prices. However, given our assessment in our recently published 2013 Mid-Year Update, showing that vessel deletions are far below expectations, owners must continue to trim their fleets in order to compensate for current and previous year’s orderbooks. If this does not occur and spot rates remain depressed, vessel values will not rebound. Vessel’s in the range of 20 years or older should be a prime candidate for deletion on the grounds of technical restrictions and vetting requirements. Although some of these older vessels are likely to be free of financing costs, slashing tonnage availability may be the only way to help rates rebound and increase earnings in the face of tepid demand.

When it comes to retail therapy, there is always the risk of the patient coming down with a case of buyer’s remorse. Today’s shipping market will not offer immediate satisfaction, unlike making a purchase on New York’s Fifth Avenue. It is much easier to return a pair of shoes than discard an oil tanker, meaning that market participants should step into orders with caution.

Editorial Standards · Corrections · About gCaptain

Join The Club

Join The Club