(gCaptain) – One presenter at a recent seminar, produced jointly by law firm Reed Smith and class society DNV, Jakub Walenkiewicz, the Principal Market Analyst at DNV, posited that recent major market developments have been driven more by disruption than anything else.

Disruption, by definition, can’t be forecast. Reinforcing his emphasis on the supply side of shipping, where “nameplate” capacities have been stretched in recent years, Walenkiewicz said: “We’ve been fueling the shipping markets with miles….” This new market visage, outlined by Walenkiewicz, is in sharp contrast to conventional “microeconomics” — with models built around developments in predicted demand for commodities moving in vessels (the stuff that economists typically try to predict and then develop forecasts around).

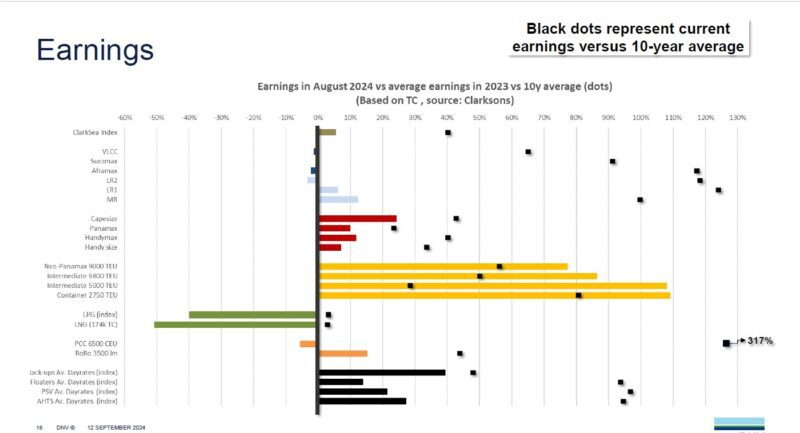

In his opening remarks and alluding to all types of uncertainties outside the realm of conventional supply/demand analytics, he offered that: “History teaches only one thing. It has never taught anyone anything.” In his data-rich presentation slides, he looked at developments which have propelled shipping markets, notably tankers, along with containerships, in recent years. These included the Russian invasion of Ukraine in early 2022, and then the Red Sea disruptions beginning in late 2023. At this point, he said that: “Shipping is absolutely swamped with cash.” In one of his slides, he showed current earnings for a variety of ship types in Q3 2024, compared to averages for the previous 10 years — showing the huge accumulations of cash. “It’s not a pure supply and demand…it doesn’t come from a solid growth of the economy.”

He described the vast cash surpluses accruing to container operators as Covid changed spending patterns (leading to great inefficiencies) before moving on to the tanker market — which had boomed with longer voyages brought about by cargo flows shifting as a result of the Ukraine war. “Ton-miles were driven absolutely through the roof,” he said, “for a fleet that was not ready to produce that much productivity.” He cited statistics, comparing 2024 with 2021, showing crude oil ton-miles up 6% and refined product ton-miles up 12%. Alluding to the shadow fleet (or “parallel” fleet) hauling Russian oil contravening sanctions, he said “Now, almost 20% of the tanker fleet is on the other side of the fence.” In discussing gas tankers — many of which saw longer routings because of drought-related restrictions at the Panama Canal — he reiterated: “It’s a miles-driven market.”

In the analysis, Walenkiewicz debunked the traditional shipping market notion that the market cycle consists of “one good year and, subsequently, seven bad years”. He asked, rhetorically, “How often do you have a situation where nearly every part of the market is earning at levels above its ten-year average?” Even in the face of reduced vessel scrapping, this has led to an overheated newbuild market (with orders for containerships and gas carriers crowding out other categories) — where resales of fairly new vessels are actually fetching prices above newbuild (where there is a multi-year wait for deliveries of the ships), as well as vessels actually speeding up (to grab some of those nearby cash flows).

Zooming in specifically on the wet sector, he said: “This is why people decide to go after tankers…it is not unreasonable to think — if you get yourself a super-efficient vessel, in three years’ time from now, and you don’t have to even bet on very strong markets — let them just stay where they are, not much growth in terms of tons, you most likely will be…able to run the vessel with much higher time-charter or spot rates.”

The brief reprieve in Red Sea shipping attacks ended this weekend as Yemen's Houthi movement signaled an imminent return to targeting commercial vessels, casting a shadow over what had been a fragile recovery in one of the world's most critical maritime corridors.

There are moments when geopolitics feels distant from daily life. This is not one of them. By Paul Morgan (gCaptain) – With confirmed US–Israeli strikes on Iran, renewed Houthi threat...

Less than a month after restarting limited Red Sea transits, Maersk is once again rerouting select services around the Cape of Good Hope, underscoring how fragile the industry’s return to the Suez corridor remains.

February 27, 2026

Total Views: 1495

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 107,166 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 107,166 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club