/Montenegro

While the sizzling summer months are coming to a close and cooler weather is beginning to set in in the North East United States, political tension in the Middle East and North Africa are causing the mercury to rise and “hot spots” are being ignited. As with many aspects of the energy sector, the impact of these types of events could be fast and far reaching.

The situation in Egypt has escalated faster than anticipated with the cost of human life catching many by surprise. Recent activities in the country suggest that the polarization of political colors will not abate in the near-term. Tempers have been flared during what is traditionally a time of unity throughout the region while political allies around the globe are starting to reevaluate their positions as a result of these developments.

These actions are all the more relevant to the global economy and the tanker industry due to Egypt’s vital role in the world’s energy market.

According to the US Energy Information Administration (EIA) the Suez Canal, which connects the Red Sea to the Mediterranean Sea, and the Sumed (Suez-Mediterranean) pipeline accounted for 7% and 13% of seaborne trade of oil and LNG in 2012. According to Suez Canal Authority, some 1.4 million b/d of crude oil transited the Suez Canal in 2012 while the Sumed pipeline pumps around 2.4 million b/d from the Red Sea to the Mediterranean.

As the situation in Egypt has the potential to worsen, market participants will stay tuned if the disputes move closer towards these installations, with potential threats including sabotage to the pipeline, industrial action, or any degree of disruption to transportation activity at the Suez Canal.

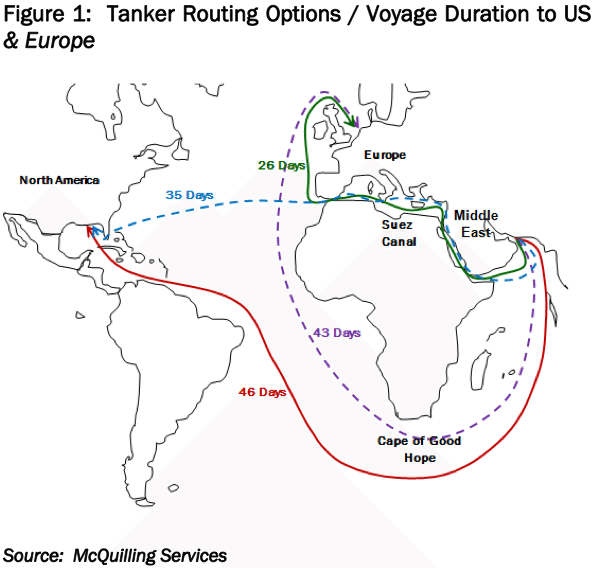

For the purpose of this note, we will assume that approximately 800,000 b/d of crude oil was sent through the Suez Canal to North America and the balance around the Cape of Good Hope. For Europe, we assume that 1.5 million b/d transit the Suez Canal. If there were any disruptions to transit through the Suez Canal, an additional 35 VLCCs would be required, under the assumption of a roundtrip voyage at 13 knots and five port days to these regions. The impact on transit times from rerouting are illustrated in Figure 1.

We recognize that any such disruptions would not be limited to crude oil movements, and would impact a range of trades and vessel classes and tighten global tonnage availability. At present, Egypt is providing some 80,000 troops to ensure that security remains tight around the Suez Canal.

The situation in Libya is another area of rising concern. Following the revolution in 2011 and the drastic fall in oil output, the rebound to pre-war production levels was rapid and returned to around 1.6 million b/d in 2012. However, since the start of 2013, various groups within the country appear to be finding ways to disagree, leading to a steady disruption of operations at ports, refineries and oil fields. Reports from Libya’s National Oil Company indicate that Libya’s oil production could have dropped to as low as 200,000 b/d. The latest production area to be disrupted from protests is the El Feel field.

In recent weeks, industrial action at oil terminals that include Ras Lanuf, Es Sider, Zueitina and Marsa al Hariga have continued to hamper exports. The employees of the company that operates these terminals, which is a subsidiary of the National Oil Company, are demanding better working conditions and higher compensation. At the end of last week, exports from Brega resumed, with the Vallesina, reportedly sailing to Italy with a cargo of crude oil. The first VLCC shipment is scheduled to load around the end of the month. Meanwhile Es Sidir, Ras Lanuf, Hariga and Zueitina remain shut. There have even been reports that a tanker was fired at while attempting to load a cargo earlier this month.

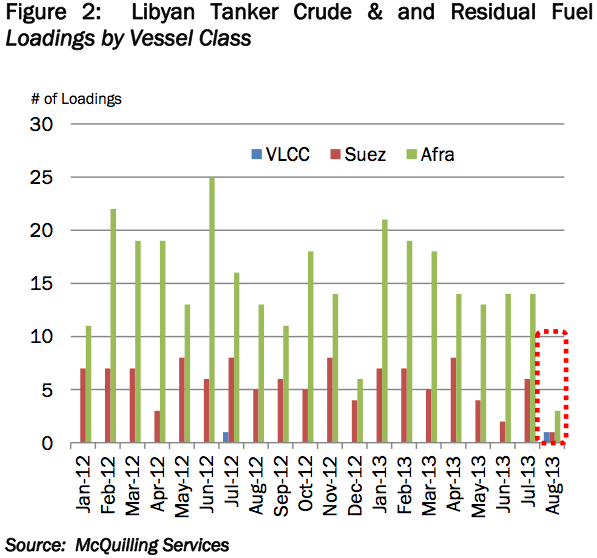

Libya is an important market for Aframax classed tankers in the Mediterranean and the impact of the recent industrial action is clear as our proprietary data shows a 70% decline in fixture activity thus far in August (Figure 2).

Libya’s petroleum product balance should also start coming under pressure as only three out of its five refineries are operating, with a combined capacity of only 150,000 b/d. The country’s largest refinery, Ras Lanuf, with a capacity of 220,000 b/d remains closed. However, the port closures could make this difficult, if not impossible.

In Iraq, continued strikes on pipeline infrastructure are reducing export volumes through Kirkuk in the North of the country. This lower export capacity, which is discharged in the Turkish port of Ceyhan, will impact Suezmax and Aframax loading schedules. According to the EIA, Iraq exported 2.4 million b/d last year, with roughly 300,000 b/d moving through Ceyhan. Through May, the EIA put Iraq’s exports at 2.9 million b/d.

Iraq’s exports from its two Single Point Moorings at the port of Basrah will also be interrupted in the coming weeks, perhaps by up to 500,000 b/d. This will be in order to connect new metering systems to the manifold platform. Throughout September exports from Basrah could be 1.79 million b/d, which would be the lowest level since February 2012. No time frame has been given for the upgrade completions, but reports indicate that it could last up to six months. A government representative stated that tankers in Iraqi waters will be re-routed to existing export infrastructure as others will take turns being shut down and reconnected in an effort to minimize export disruptions.

Owners of large tankers should find some solace as output should rise by 400,000 b/d in the balance of the year as the Majnoon field is set to come on stream. As Iraq continues to rebuild, and sectarian tensions are on the rise, stability is anything but guaranteed.

Syria is also a country that could have a significant impact on a variety of markets. Although the country has been mired in a civil war for nearly three years, the recent revelation that chemical weapons were used against its population, again, is almost certain to result in international action. Since the revelation, which appears to be undeniable due to various sources of video footage and first hand testimony, the US and its allies have hardened their rhetoric while Syria’s allies seem to accept this new reality. Although Syria’s role in the energy markets is of little significance, a serious conflict in the country has the potential to wreak havoc and inflame other regional tensions. In terms of world oil output, the Middle East accounted for 35% in 1Q 2013, according to the International Energy Agency.

As stated in our previous industry note, For Good Measure, following the start of the global financial crisis in 2007, we expected the shipping markets to be immediately affected. The lesson learned was that the effects of major events take time to move through complex transport systems such as the tanker industry.

Although we hope it doesn’t, the current events that are heating up in various parts of the globe have the potential to provide a new measure for future forecasting reviews.

Editorial Standards · Corrections · About gCaptain

Join The Club

Join The Club