Just how much money would container shipping lines be losing if it weren’t for the relentlessly steep decline in bunker prices?

A lot, according to the latest analysis from Drewry Maritime Research, which investigated the revenues and margins of 16 of the 20 largest carriers that publish their accounts.

Drewry calculates that the group, which represented 65% of global slot capacity, saw revenue of around $60bn in the first half of the year, 5% less than in the first six months of 2014. Only Taiwanese carriers Wan Hai, a specialist on niche trades such as intra-Asia, and Yang Ming managed to increase sales year-on-year.

The decline was the result of low demand combined with low freight rates.

However, it is a mark of how decisive fuel costs have become to the liner shipping industry that, despite this decline in revenue, saw operating profits in the same period actually triple: the 16 carriers posted combined operating profits of $3.3bn, compared with $1.1bn during the first six months of 2014, as margins increased from 1.7% to 5.6% in the first half of this year.

In January 2014, the average price of one tonne of IFO380 bunker fuel bought at Singapore or Rotterdam was just under $600, a year and a half later in July, it had dropped by almost two-thirds to marginally under $250 per tonne.

Drewry wrote yesterday: “The change in direction that fuel costs has taken means that carriers’ costs are falling faster than freight rates, enabling them to continue posting profits, albeit shrinking with each passing quarter.

“Drewry estimates that industry-wide unit costs fell by about 11% in the first-half 2015 versus the same period last year, whereas unit revenues were down by approximately 7%.”

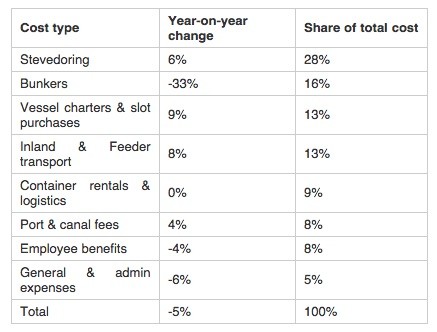

It added that while few carriers provided much insight into their cost structures, CMA CGM gave a detailed breakdown of its costs in its most recent results:

Source: CMA CGM via Drewry Maritime Research/The Loadstar

The table shows that the French Line reduced the costs over which it has direct control – wages and office expenses – but the massive influence of the 33% decline in bunker costs mitigated the fact almost every external supplier to the carrier managed to increase their revenue from CMA CGM. It further demonstrates how carriers have to gain greater control over pricing and capacity in the long-term, should fuel costs begin to ascend to previous levels; although Drewry thinks this is unlikely this year.

“Based on prevailing fuel and rates in the third quarter 2015, we expect the story will be much the same, ie diminishing profitability, meaning that the accumulation over the first nine months will be enough for carriers to walk away with okay sums for the full year, regardless of what happens in the fourth quarter.”

The Loadstar is fast becoming known at the highest levels of logistics and supply chain management as one of the best sources of influential analysis and commentary.

The nation’s two busiest container gateways continued to benefit from an early peak shipping season in June as importers rushed cargo into the United States ahead of potential new tariffs,...

By Lori Ann LaRocco – The Port of Los Angeles, the nation’s busiest container seaport, processed more than 1 million twenty-foot equivalent units (TEUs) in June, making it the busiest...

The first container ship to run on Brazilian-made ethanol fuel is scheduled to sail early Tuesday from the port of Santos, an unprecedented test for the nation’s biofuel industry that marks a key step toward cutting emissions in maritime transportation.

July 14, 2026

Total Views: 580

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 104,564 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 104,564 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club