13-19 April 2012

Another roller-coaster ride this week in the oil markets as volatility remains the only constant. A positive meeting over this past weekend between Iran, the United States, Russia, China, Britain, France and Germany had the market selling off early in the week. While no clear agreements have been made with Iran over their nuclear program they do seem to want to reach a diplomatic solution. This put more pressure on Brent than WTI as none of the Iranian crude reaches the WTI market. Additional strength in WTI prices came from the potential reversal of the Seaway Pipeline. This was expected to happen at the end of May, but there is talk that it could happen two weeks sooner. We are now seeing what used to be a $20 bbl or more difference reduced to a $15 bbl difference between Brent and WTI.

So what is going to happen when these prices converge? It is not really clear if they will reduce to WTI levels or move up to Brent levels. Logic would dictate they will end up somewhere in between, but logic seems to have left the oil markets many years ago.

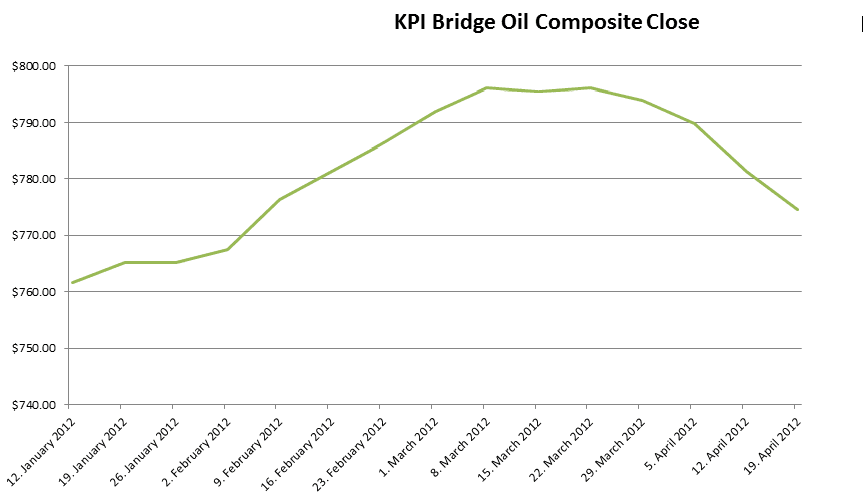

The good news is that KPI Bridge Oil Composite is showing a clear downward trend. While this does not help with timing the markets it should show on companies’ bottom lines as fuel prices are declining.

About the KPI Bridge Oil Composite

The KPI Bridge Oil Composite is a calculated fuel number based on 14 ports strategically positioned world wide. It is calculated on a weekly basis blending 90% fuel oil prices with 10% distillate prices. The idea behind the number is that it would represent actual fuel costs on a global basis and what vessels would consume on average. This number will not fluctuate as quickly as daily prices and can easily be hedged or used for voyage calculations.

The KPI Bridge Oil Composite is a calculated fuel number based on 14 ports strategically positioned world wide. It is calculated on a weekly basis blending 90% fuel oil prices with 10% distillate prices. The idea behind the number is that it would represent actual fuel costs on a global basis and what vessels would consume on average. This number will not fluctuate as quickly as daily prices and can easily be hedged or used for voyage calculations.

Editorial Standards · Corrections · About gCaptain

Join The Club

Join The Club