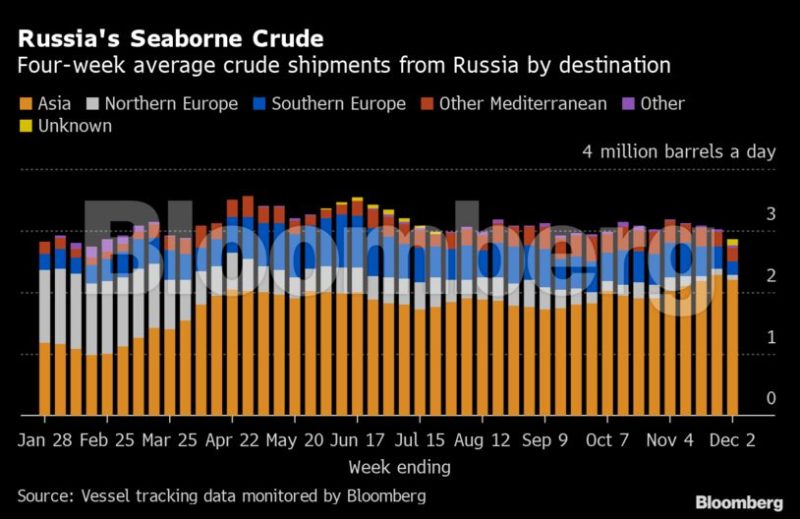

Russia’s crude oil shipments to Europe are shrinking fast. A European Union ban on seaborne imports from the country is now in effect, shutting off a market that was taking more than 1.5 million barrels a day before Moscow’s troops invaded Ukraine in late February.

The flow dropped to less than one-fifth of that volume in the four weeks to Dec. 5, and will fall close to zero once the sanctions really bite.

So far, the displaced shipments have been diverted to Asia, with a flotilla of tankers steaming around Europe and through the Suez Canal to deliver cargoes to India and China. That route has become more expensive as the EU ban and a linked $60 a barrel price cap on sales carried on the bloc’s ships or seeking insurance and other services through its companies have loomed.

Higher shipping costs have undermined the price of Russian crude at its Baltic export terminals, which has been trading more than $30 a barrel below international benchmark Brent. That will have an impact on future inflows to the Kremlin’s war chest, with the falling prices set to be reflected in the level of oil export duty payable on shipments loading in January.

In the final week before the EU ban came into effect, total volumes shipped from Russia rose by 94,000 barrels a day to 2.99 million in the seven days to Dec. 2, while the less volatile four-week average continued to slide. That latter measure fell by 153,000 barrels a day to drop below 3 million for the first time since October and to its lowest since the invasion.

The volume of crude on vessels heading to China, India and Turkey, the three countries that have emerged as the biggest buyers of displaced Russian supplies, plus the quantities on ships that are yet to show a final destination, slipped slightly in the four weeks to Dec. 2 to average 2.45 million barrels a day. That’s still three-and-a-half times as high as the volume shipped in the four weeks immediately prior to Russia’s invasion of Ukraine.

Tankers hauling Russian crude are becoming more cagey about their final destinations. The volume of crude on vessels leaving the Baltic and showing their next destination as Port Said or the Suez Canal jumped to more than 750,000 barrels a day. It remains likely that most of these vessels will begin to signal Indian ports once they pass through the canal.

Two more tankers began to signal the United Arab Emirates as their destination. The Elza and the Coatlicue both began to show Fujairah as their next port of call, though it remains unclear what will happen with their cargoes once they get there.

Crude Flows by Destination:

On a four-week average basis, overall seaborne exports recorded their biggest drop since September, falling by 153,000 barrels a day and declining below 3 million barrels a day for the first time in eight weeks. Shipments to Europe hit a new low for the year, while those to Asia were little changed.

All figures exclude cargoes identified as Kazakhstan’s KEBCO grade. These are shipments made by KazTransoil JSC that transit Russia for export through Ust-Luga and Novorossiysk.

The Kazakh barrels are blended with crude of Russian origin to create a uniform export grade. Since the invasion of Ukraine by Russia, Kazakhstan has rebranded its cargoes to distinguish them from those shipped by Russian companies. Transit crude is specifically exempted from the EU sanctions.

Europe

Russia’s seaborne crude exports to European countries fell to 309,000 barrels a day in the 28 days to Dec. 2, taking them to less than one-fifth of the levels seen before the invasion. Flows were down by 156,000 barrels a day, or 34%, from the period to Nov. 25. These figures do not include shipments to Turkey.

The volume shipped from Russia to northern European countries remained at the previous week’s low, with Rotterdam still the only destination for deliveries to the region. Flows were 95,000 barrels a day in the four weeks to Dec. 2, down from more than 1.2 million barrels a day pre-invasion.

Exports to Mediterranean countries slipped to 303,000 barrels a day on average in the four weeks to Dec. 2, hitting their lowest level since Moscow’s attack and down from 485,000 barrels a day in the same period to Nov. 25. Flows to the region, including Turkey, which is excluded from the European figures at the top of this section, fell for a fourth week.

Shipments to Italy slumped to just 52,000 barrels a day, their lowest level for the year so far. The country’s largest refinery, the ISAB plant in Sicily owned by Lukoil PJSC, has been struggling to secure credit to buy crude. It has been processing Lukoil’s own crude, much of it shipped from the Arctic, but that flow will now have to stop, with EU sanctions on seaborne imports of Russian crude coming into effect.

The plant could come under temporary Italian government administration to guarantee continuity of operations, but it won’t be nationalized, according to Industry Minister Adolfo Urso. Lukoil said that its Litasco SA unit is prepared to guarantee operations at the ISAB refinery using crude stored for the coming months and future deliveries of non-Russian supplies.

Flows to Turkey also fell, dropping to their lowest since July on a four-week average basis. However, they remain more than twice the volume typically seen before the invasion, and the country is expected to continue to be an important destination for Russian crude going forward.

Flows to Bulgaria, now Russia’s only Black Sea market for crude, were unchanged at 125,000 barrels a day. Bulgaria secured a partial exemption from the EU ban on seaborne crude imports from Russia, which should support inflows as the embargo comes into force. However, it remains unclear whether a proposed Russian ban on sales to countries that participate in the US-led price cap mechanism will affect shipments to the country.

Asia

Shipments to Russia’s Asian customers, plus those on vessels showing no final destination, which typically end up in either India or China, were little changed from the previous week. While the volume on vessels signaling Indian ports as their destination slumped, the number of ships showing destinations as either Port Said or Suez soared to the equivalent of more than 750,000 barrels a day. Those voyages typically end at ports in India and show up in the chart below as “Unknown Asia,” as do the volumes expected to be transferred from one ship to another off the South Korean port of Yeosu.

The “Unknown” volumes are those on tankers showing a destination of Gibraltar, Malta or no destination at all. Most of those cargoes go on to transit the Suez Canal, but some could end up in the Mediterranean region.

The total volume of crude expected to end up in Asia remained at 2.28 million barrels a day on a four-week rolling average basis, including 89,000 barrels a day on tankers whose point of discharge is unclear. Cargoes heading for Asia that were bought at a price above $60 a barrel at the point of loading will have to be delivered before Jan. 19, if they are to retain their International Club insurance. Alternative insurance arrangements will need to be made for any cargoes that are discharged after that date.

Flows by Export Location

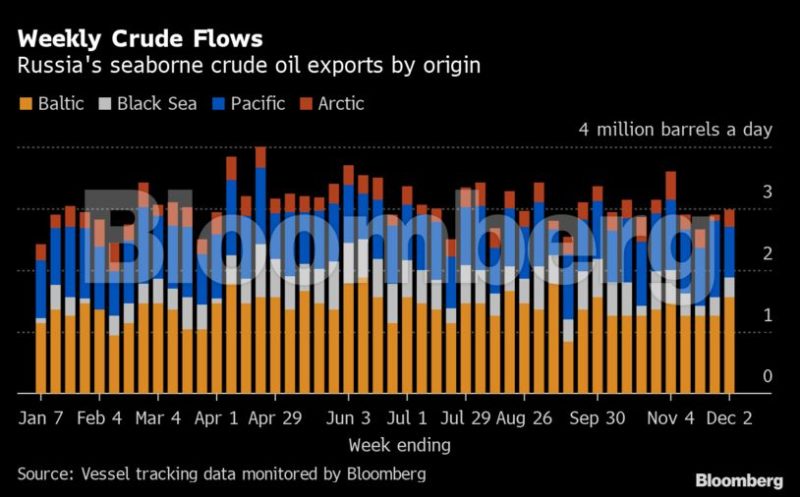

Aggregate flows of Russian crude rose by 94,000 barrels a day, or 3%, in the seven days to Dec. 2, to nudge just below 3 million barrels a day. Shipments from western ports in the Baltic, Black Sea and the Arctic all rose, while exports slumped from the Pacific port of Kozmino. Figures exclude volumes from Ust-Luga and Novorossiysk identified as Kazakhstan’s KEBCO grade.

Export Revenue

Inflows to the Kremlin’s war chest from its crude-export duty rose by $4 million to $122 million in the seven days to Dec. 2, while the four-week average income continued to drop, falling by $7 million to $117 million. The four-week average hit a new low for the year so far.

The November duty rate was $5.83 a barrel, the lowest level since January 2021, but the December rate is 8 cents a barrel higher at $5.91, according to figures released by the Russian Ministry of Finance. This month’s figure is based on an average Urals price of $71.1 a barrel, according to figures from the Russian Ministry of Finance. The duty rate for January could be much lower, with Urals prices falling in the Baltic to about $52 a barrel 10 days into the January calculation period, which runs from Nov. 15 to Dec. 14.

Origin-to-Location Flows

The following charts show the number of ships leaving each export terminal and the destinations of crude cargoes from the four export regions.

A total of 28 tankers loaded 20.9 million barrels of Russian crude in the week to Dec. 2, vessel-tracking data and port agent reports show. That’s up by 665,000 barrels, or 3%, from the previous week. Destinations are based on where vessels signal they are heading at the time of writing, and some will almost certainly change as voyages progress. All figures exclude cargoes identified as Kazakhstan’s KEBCO grade.

The total volume on ships loading Russian crude from Baltic terminals rose to a nine-week high of 1.56 million barrels a day in the week to Dec. 2. One tanker, the Alma, is showing its destination as Rotterdam and an arrival date as Dec. 6, one day after the EU import ban comes into effect. For the first time this year, there are no cargoes on ships showing destinations in the Mediterranean, though there are tankers showing no destination that could end up discharging in the region.

The jump in shipments from the Baltic could reflect an attempt to load cargoes for Asia before the EU ban on insuring Russian cargoes bought at a price above the $60 a barrel cap came into effect. Cargoes loaded before Dec. 5 can still obtain International Club insurance as long as they are delivered before Jan. 19.

Shipments from Novorossiysk in the Black Sea were unchanged from the previous week. All of the ships showing a destination remained within the Black Sea, but two tankers are yet to signal a discharge point and could yet leave the area.

Arctic shipments rebounded in the seven days to Dec. 2 with two vessels leaving from Murmansk during the week. Both are heading to Asia via the Suez Canal.

Shipments from the Pacific slumped to a 12-week low in the seven days to Dec. 2. All of the cargoes heading for unknown destinations are on ships going to Yeosu in South Korea, where it’s likely that they will conduct ship-to-ship transfers outside the port, as previous tankers have done. All cargoes of Sokol crude loaded since shipments restarted in October have been moved in this way, with most eventually heading to India.

The U.S. Treasury Department has quietly extended its sanctions wind-down authorization for Russian oil cargoes already at sea, issuing a new general license that allows shipments to continue flowing through...

Two fully laden Chinese oil tankers are waiting near the Strait of Hormuz with a third on its way, putting them in a position to become the first such vessels to leave the Persian Gulf under a day-old US-Iran ceasefire, even as shipowners scrutinize the details of the truce.

By Eric Martin and Scott Squires Mar 29, 2026 (Bloomberg) –The Trump administration is planning to let a Russian oil tanker dock in Cuba, alleviating an energy crisis triggered when the...

March 29, 2026

Total Views: 1878

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 106,013 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 106,013 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club