A day after dry bulk shipper Genco Shipping announced filing for Ch. 11 bankruptcy protection, the Baltic Dry Index (BDI) continues to fall further.

At 930 points, it’s less than half of where it was at the end of December 2013.

The BDI is a simple measurement of the balance between the demand for shipping capacity and the supply of dry bulk ships and factors-in the daily time-charter rates for Capesize, Panamax, Supramax and Handysize bulk carriers. Demand for dry bulk shipping is largely driven by China, a country which is now entering a period of reduced GDP growth, and thus lower demand for dry bulk shipping.

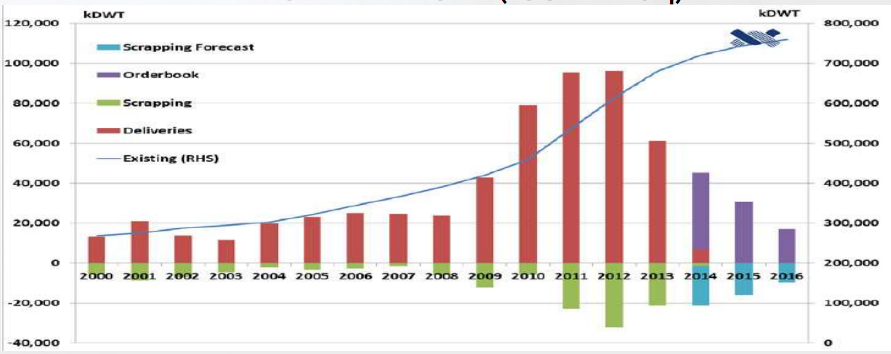

Dry bulk fleet profile as of February 2014, source: Fernley’s

The above graph, posted in Singapore-based Mercator Lines’ 2014 Annual Presentation shows that although deliveries of new bulk carriers are expected to be significantly lower in the coming years, the global fleet is continuing to grow. This fleet growth is mainly due to the influx of cash into the market led by private equity firms according to Mercator.

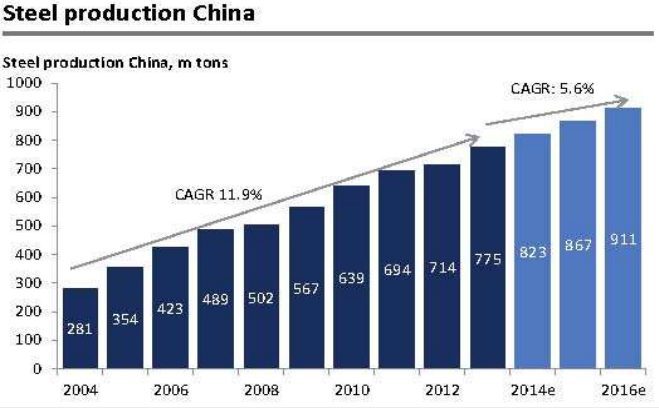

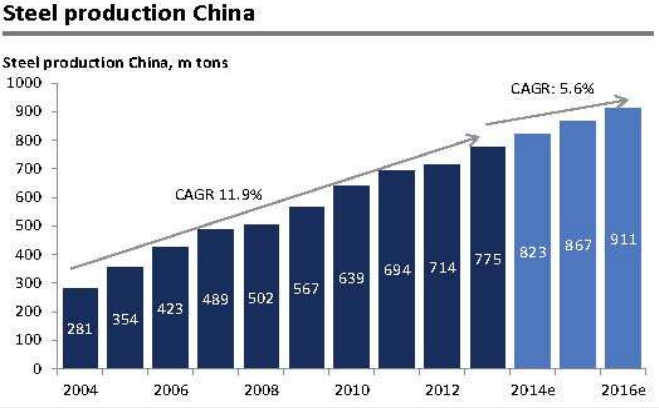

Data from Pareto also shows that going forward, the compounded annual growth rate (CAGR) of China’s steel production is predicted to be half of what it has been over the past decade, further exacerbating overcapacity problems facing the capesize shipping market.

Source: Pareto

In Safe Bulkers’ 2013 Annual report released in March, they note:

“The market supply of drybulk vessels has been increasing, and the number of drybulk vessels on order as of December 31, 2013, was approximately 21.4% for Panamax class vessels, 12.6% for Post-Panamax class vessels and 20.0% for Capesize class vessels of the then-existing global drybulk fleet in terms of deadweight tons (dwt), with the majority of new deliveries expected mainly during 2014 and 2015.

As a result, the drybulk fleet continues to grow.”

According to a report by Clarksons last month, the dry bulk fleet has grown 6 percent since 1 January 2013.

Although the dry bulk fleet is growing, the market demand for this added capacity continues to grow as well. In a report released recently by MIDF, the 2013 year-on-year growth in demand was up 7 percent.

It’s important to note however that during that same period, China’s GDP growth was at 7.7 percent and the year prior it was 7.8 percent. This number is projected by the IMF to fall however, to 7.5 percent in 2014 and 7.3 percent in 2015.

How exactly all of this will translate into the dry bulk sector is anyone’s guess, but it does not look like news of a greater sector recovery.

Dry bulk shipping takeover drama intensified Thursday as Diana Shipping Inc. raised its all-cash offer for Genco Shipping & Trading Limited to $24.80 per share, increasing pressure on Genco’s board...

Danish shipping giant D/S NORDEN says the ongoing Persian Gulf conflict and disruption to the Strait of Hormuz are having sharply different effects across global shipping markets, hammering dry cargo...

Longer average sailing distances are expected to support dry bulk demand through 2026, helping offset rising fleet growth and keeping market conditions relatively stable before weakening in 2027, according to...

January 29, 2026

Total Views: 375

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 105,559 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 105,559 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club