Editor’s Note: A.P. Møller – Mærsk A/S published its Interim Report for Q3 2016 on Wednesday, 2 November 2016, reporting that its third quarter profit fell 44 percent to US $426 million. Of note, Maersk said its flagship container unit, Maersk Line, sank to a net loss of $116 million due to falling freight rates. Here’s the full press release from Maersk Group:

Photo: Maersk Group

Highlights:

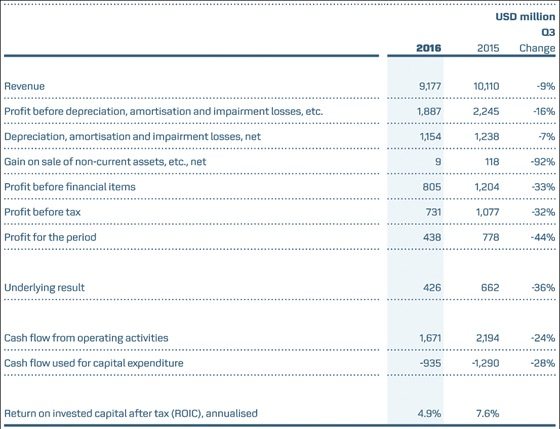

The Maersk Group delivered an underlying profit of USD 426m in the third quarter of 2016.

All business units generated free cash flows of a total of USD 736m and the Group maintains a strong financial position with a liquidity reserve of USD 11.8 bn.

The result was positively impacted by continued strong operational performance and cost reductions in both Maersk Oil and Maersk Drilling.

Maersk Oil increased underlying profit through continued operational efficiency increases and cost reductions and break-even is now reduced to below USD 40 per barrel for 2016.

Maersk Line gained market share with a volume growth of 11%, while continuing to improve network utilisation and maintaining unit costs below 2,000 USD/FFE.

APM Terminals lifted Q3 performance from previous quarters due to stronger performance in key gateway terminals and cost saving initiatives.

The Group still expects a result significantly below last year (USD 3.1bn) and specifies an expected underlying result below USD 1.0bn.

The Group continued to be significantly impacted by market imbalances, leading to sustained low container freight rates and a low oil price environment.

The Group delivered a profit of USD 438m (USD 778m) negatively impacted by lower container freight rates partly offset by positive impact of termination fees in Maersk Drilling. The return on invested capital (ROIC) was 4.9% (7.6%). The free cash flow was USD 736m (USD 904m).

The underlying profit for the Group of USD 426m (USD 662m) was significantly lower than for same period last year, predominantly driven by a loss in Maersk Line and with lower underlying results in APM Shipping Services and APM Terminals. Maersk Drilling and Maersk Oil recorded increased underlying profits.

The Group continues to focus on cost efficiency as well as maximising synergies between our business units to improve operational performance and remain top tier performer.

“The Maersk Group delivered an underlying profit of USD 426m in the third quarter of 2016. The result is unsatisfactory, but driven by low prices. We generally perform strongly on cost and volume across businesses. Maersk Line for the second quarter in a row reported a loss due to continued low freight rates, down 16% y-o-y. Freight rates were however up 5.5% q-o-q, for the first time since Q3 2014. Maersk Line performed strongly on volume and unit cost. APM Terminals delivered a result below last year, as we continued to be challenged by low volume growth on a like–for-like basis. For the second quarter in a row Maersk Oil delivered a positive result driven by strong cost performance and production efficiency. Also Maersk Drilling delivered strong profits, driven by termination fees and good cost performance. The implementation of the new strategic direction and the restructuring of the Group is progressing, and we look forward to sharing further details at the Capital Markets Day on 13th of December,” says Maersk Group CEO Søren Skou.

Group Highlights:

The Group’s revenue decreased by USD 933m or 9.2% compared to Q3 2015, predominantly related to Maersk Line with a decrease of USD 659m due to 16% lower average container freight rates, Maersk Oil with a decrease of USD 95m due to 8.0% lower oil prices and decreased rates in Damco and Maersk Tankers. This was partly offset by 11% higher container volumes in Maersk Line and 7.0% higher volumes in APM Terminals.

Operating expenses decreased by USD 573m or 7.3% mainly due to lower bunker prices and cost saving initiatives.

The Group’s cash flow from operating activities was USD 1.7bn (USD 2.2bn). Net cash flow used for capital expenditure was USD 935m (USD 1.3bn) with investments predominantly related to developments of the Culzean oil field in the UK and Johan Sverdrup in Norway.

With an equity ratio of 55.5% (57.3% at 31 December 2015) and a liquidity reserve of USD 11.8 bn (USD 12.4bn at 31 December 2015) the Group maintains a strong financial position.

Maersk Line continued to deliver on strategic objectives in Q3, gaining market share with a volume growth of 11% and continued improvement in network utilisation. Sustained pressure on container freight rates lead to a decline in average freight rates of 16% and an underlying loss of USD 122m. However, Maersk Line generated a positive free cash flow of USD 192m (USD 159m).

ROIC was negative 2.3% (positive 5.2%). The result was favourably impacted by various positive tax developments.

Revenue of USD 5.4bn was 11% lower than Q3 2015. The development was driven by a 16% decline in average freight rates to 1,811 USD/FFE (2,163 USD/FFE) partially offset by an 11% increase in volumes to 2,698k FFE (2,427k FFE). A significant part of the growth was due to more backhaul cargo at lower rates than headhaul. With an increase in fleet capacity of 3.8%, the increase in volumes represented an improvement of network utilisation. The freight rate decline was mainly attributable to decreasing bunker prices of 25%, but was also impacted by the increased backhaul volumes and continued weak market conditions.

Maersk Oil continues to deliver profit in a quarter with an average oil price of USD 46 per barrel and with a breakeven level below USD 40 per barrel for 2016. Adjustments to the business and organisation due to lower oil price environment and exit from Qatar by Mid-2017 have been initiated.

Maersk Oil reported a profit of USD 145m (USD 32m) and a ROIC of 13.5% (2.1%) in Q3 2016 at an oil price of USD 46 (USD 50) per barrel. The profit was positively impacted by higher operational efficiency and lower costs.

In a quarter with the usual planned maintenance shutdowns, entitlement production of 295,000 boepd (300,000 boepd) was in line with Q3 2015. Exploration costs of USD 57m (USD 82m) were 30% lower than the same period last year.

APM Terminals delivered a profit of USD 131m (USD 175m) and a ROIC of 6.6% (11.6%). Stronger performance in key gateway terminals lifts Q3 performance from previous quarters in 2016 while cost saving initiatives are starting to offset some of the reduced volume in commercially challenged terminals.

The profit was 17% above Q2 2016. Operating businesses generated a profit of USD 136m (USD 189m) and a ROIC of 9.5% (13.8%) and projects under implementation along with Grup Marítim TCB from beginning of March had a combined loss of USD 5m (loss of USD 14m), resulting from start-up costs. Profits remain under pressure in commercially challenged terminals in Latin America, North-West Europe and Africa as a consequence of liner network changes and continued weak underlying market conditions.

Maersk Drilling delivered a profit of USD 340m (USD 184m) and a ROIC of 17.2% (9.0%). Termination fees, high operational uptime and savings on operating costs were partly offset by more idle days. Underlying profit was positively impacted by USD 210m from early contract termination of Maersk Valiant.

Maersk Drilling has benefitted from a strong contract coverage at significantly higher dayrates than offered in the current market, but the market outlook for the offshore drilling industry remains challenged, which will also affect Maersk Drilling going forward as current contracts expire and new low dayrates are adopted or rigs are idle.

APM Shipping Services reported a profit of USD 25m (USD 154m) and a ROIC of 2.1% (13.1%) negatively impacted by a loss of USD 11m (profit of USD 45m) in Maersk Supply Service and a loss in Maersk Tankers of USD 1m (profit of USD 59m).

Maersk Tankers reported a loss of USD 1m (profit of USD 59m) and a negative ROIC of 0.3% (positive 14.6%). The result was negatively affected by deteriorating market rates (decrease of 59%), partly offset by Maersk Tankers market outperformance, contract coverage and cost saving initiatives aimed at creating higher efficiencies.

Maersk Supply Service reported a loss of USD 11m (profit of USD 45m) and a ROIC of negative 2.5% (positive 10.4%). Revenue for Q3 decreased to USD 94m (USD 145m) following lower rates and utilisation as well as fewer vessels available for trading due to divestments and lay-ups. Total operating costs increased to USD 72m (USD 69m), as a result of crew redundancies partly offset by fewer operating vessels and reduced running cost. Maersk Supply Service is well on the way of reducing daily running costs by a double digit percentage compared to 2015 on a like-for-like basis.

Svitzer delivered a profit of USD 22m (USD 30m) and a ROIC of 6.9% (10.8%). Despite new terminal towage activity in Australia and Americas and higher harbour towage activity, revenue saw only marginal increase of USD 2m. Positive effects were offset by low utilisation of the terminal towage spot fleet and GBP exchange rate impact. Even with significant over-capacity and slowdown in most shipping segments, Svitzer maintained its market share in competitive ports both in Australia and Europe.

Damco delivered a profit of USD 15m (USD 20m) and a ROIC of 29.7% (30.0%). Revenue was USD 635m (USD 719m), down 12%, impacted by lower freight rates and rate of exchange movements. Margins in supply chain management improved, while freight forwarding margins remained under pressure.

The Group’s guidance for 2016

In line with previous expectations the Group still expects a result significantly below last year (USD 3.1bn) and specifies an expected underlying result below USD 1.0bn. Gross cash flow used for capital expenditure is still expected to be around USD 6bn in 2016 (USD 7.1bn).

Maersk Line still expects an underlying result significantly below last year (USD 1.3bn) and specifies an expected negative underlying result for 2016. Maersk Line expects global demand for seaborne container transportation to increase by around 2% in line with previous expectation of 1-3%.

Maersk Oil still expects a positive underlying result. A breakeven result is now expected to be reached with an oil price below USD 40 per barrel versus previously in the range of USD 40–45 per barrel.

Maersk Oil maintains an expected entitlement production of 320,000-330,000 boepd (312,000 boepd), and exploration costs significantly below last year (USD 423m).

APM Terminals still expects an underlying result significantly below 2015 (USD 626m), due to reduced demand in oil producing emerging economies and network adjustments by customers.

Maersk Drilling now expects an underlying result in line with last year (USD 732m), with a break-even result expected in Q4, versus previously an underlying result below last year.

APM Shipping Services reiterates the expectation of an underlying result significantly below the 2015 result (USD 404m) predominantly due to significantly lower rates and activity in Maersk Supply Service and weaker rates in Maersk Tankers.

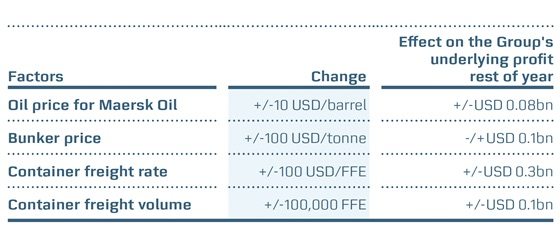

The Group’s guidance for 2016 is subject to considerable uncertainty, not least due to developments in the global economy, the container freight rates and the oil price. The Group’s expected underlying result depends on a number of factors. Based on the expected earnings level and all other things being equal, the sensitivities for the calendar year 2016 for four key value drivers are listed in the table below:

Group strategy update

The Group initiated a strategic review on 23 June to evaluate the strategic and structural options with the objective to generate growth, increase agilities, unlock synergies, and maximise shareholder value. The Group announced a progress update on the strategic review on 22 September.

The future Maersk Group will be an integrated transportation and logistics company, while the objective is to find structural solutions for each of the oil and oil related companies. The Maersk Group will going forward deliver best in class transport and logistics services as an integrated company based on combined capabilities, supported by industry leading digital solutions.

As a consequence the Group’s portfolio will be reorganised into two separate divisions: Transport & Logistics and Energy. The Transport & Logistics division consists of Maersk Line, APM Terminals, Damco, Svitzer and Maersk Container Industry. The Energy division consists of Maersk Oil, Maersk Drilling, Maersk Supply Service and Maersk Tankers.

The Transport & Logistics division will focus on generating growth and synergies based on a one company structure with multiple brands, by managing and operating the activities in a more integrated manner. The strategy of Transport & Logistics rests on three pillars to deliver long term profitable growth:

Product offering and customer experience will be improved based on the combined capabilities of Maersk Line, APM Terminals and Damco in combination with industry leading digital solutions.

By operating as one entity, Transport & Logistics will be able to harvest synergies and optimise operations to secure the industry’s most effective and reliable network.

Strong capital discipline and better utilisation of assets will be ensured. When making investments, acquisitions will be the preferred option.

The estimated synergies are expected to generate up to two percentage points ROIC improvement over a period of three years. No material synergies are expected in 2016. It is expected that the oil and oil related businesses within the Energy division will require different solutions for future development including separation of entities individually or in combination from A.P. Møller – Mærsk A/S in the form of joint-ventures, mergers or listings. Depending on market development and structural opportunities, the objective is to find solutions for the oil and oil related businesses within 24 months.

The Board of Directors continues to focus on ensuring a strong capital structure and defined key financial ratio targets in line with an investment grade rating.

Financial reporting for the new structure will be effective as of Q1 2017.

At nearly 40 years old, Lars Jensen’s Volkswagen camper van appeals to him mostly for its lack of modern features. The vehicle he calls “Sally” is just the right rig to drive around Africa over the next 18 months to explore the world’s most promising supply chain frontier.

The U.S. Federal Maritime Commission has secured a $1.9 million civil penalty settlement from Danish shipping giant A.P. Moller – Maersk over allegations the carrier improperly billed third parties for detention charges...

Container shipping giant Hapag-Lloyd reported a sharp deterioration in first-quarter earnings on Tuesday, blaming severe weather disruptions and the conflict in the Middle East for rising costs and weaker operational performance as...

May 13, 2026

Total Views: 497

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 105,215 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 105,215 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club