The main concern at Vale S.A., that which has driven its order of dry bulk vessels with a 400,000 ton capacity, the ‘Valemax’, is competition…

The problem is obvious – it costs a great deal more to send a “Capesize” ship from Brazil to China, by far the largest importer of iron ore, than it costs to ship from Australia, a major source for mining competitors Rio Tinto and BHP Billiton. Vale saw economy of scale per ships double the size of the cape vessels: one ‘Valemax’ equaling more than 2 Capesize ships.

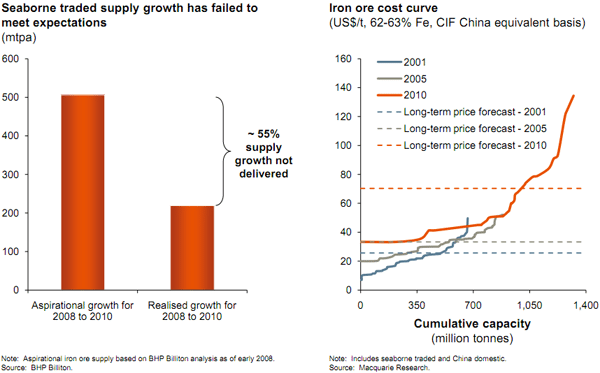

Supply likely to under perform, steep cost curve underwrites growth plan, courtesy BHP Biliton

Vale has some advantages in competition

Courtesy BHP Billiton

Vale produces better iron ore which makes production at the steel mills more efficient, and thus cheaper. In addition, Australian miners are annually dealing with damage from rain and floods; damage that amounts to nothing less than impaired capital investment and months of delays and shut downs. Furthermore, delays at Australian ports are notoriously long and therefore, if the ship is leased at a daily rate, extremely expensive. During the 10 months running up to the crash of 2008, the Baltic Dry Index (BDI) was often over 11,000. Ships were leased at astronomical fees. Regardless of the hike in ore prices, this exacerbated the distance issue for Vale. It also made port delays into 7-figure money pits.

I think Vale wants to develop vertically, that is, to own all the elements of their business short of milling the steel. They own their own railroad from the mines to the ports and they obviously own the ore from their mines. What if they owned their own ships and developed their own ports? Whatever prices they would have paid to third party services would be sunk into the company as capital investment; renting vs. owning… and that was what they were doing. They are building new ports and are reengineering others in Brazil. They are moving forward with plans to build hubs in Malaysia and the Philippines to use as a springboard to their Asia trade; again the logistic issue.

Vale determined that the ship leases running up to September 2008, given the time of travel and the length of delays, were killing their profits. That is where this whole ‘Valemax’ vessel scheme came from; economy of scale.

Vale is not alone in going vertical.

So they make a deal with Chinese ship builders for these ships at well over a billion dollars. Good for China right? Good for the ship builders and for the steel mills and for their economy in general. Then the China Shipowners Association wants to prevent Vale from delivering their product to China in these very ships…

As far as I can tell, Chinese shipping companies are woefully and even utterly incompetent. COSCO is a good example.

How can that local shipping company with immediate access to international, regional, coastal and even interior trade and the benefactor of a 451 +/- ship deal [more like a steal] via the government be losing money?

Incompetence? Corruption?

I’ll give COSCO the benefit of the doubt and say it is simply pathetic. And this Association wants the Chinese steel industry to use COSCO et al. and not Vale; Vale through whom it would benefit from a well-run company with a known reputation shipping superior product with that economy of scale?

Should I mention the basically squirrelly nature of the shipping industry? And the well known weirdness of the iron ore market – mostly imposed on China by its own hand – which would beg the question, wouldn’t the stability of the ‘verticalized’ Vale be of benefit sooner, if not later?

Finally, this can’t be good for trade relations down the road. it reminds me of when Goldman Sachs recently took massive short positions on an investment that they knew was crap and then sold the long positions to clients.

I’d like to have been in the room at Vale when they got this this news from that shipping association… and i’m guessing there were many unhappy faces in boardrooms and government offices in China as well.

Perhaps there is some subtext significance in this deal; a backhanded attempt by China to manipulate Brazilian policy in some way to some end. Otherwise it doesn’t add up to anything but the improbable and idiotic scenario as I laid it out above. (look for a dearth of international ship orders to Chinese ship builders.)

A day after I wrote the above, lo and behold the Valemax ship Berge Everest berthed at the port of Dalian and began the 2 1/2 day job of disgorging its cargo of 388,000 tons of first-rate Vale iron ore. Coincidentally, the Chinese Shipowners Association Vice Executive Chairman, Zhang Shouguo, published another Association negative opinion stating Vale’s shipping model is not only anti-competitive, but is a waste of resources and counterintuitive per the basic rules of capitalism.

Mr. Zhang wants to save Vale from itself.

This is a little bit beyond belief. Unless I am missing something, part of the problem in the Chinese Shipowners Association (CSA) is their lack of experience in capitalism. I recall that during the negotiations on iron ore price contracts, the Chinese Iron and Steel Association (CISA) screwed up royally; a screw-up that is still costing Chinese steel mills a fortune to date.

CISA too spoke of the irrationality of the ore producers demands inasmuch as the miners did not recognize the principle that only a bargain that is fair to both sides would be the rational and most profitable way of preceding, e.g sound capitalism.

They clearly have not yet absorbed two important concepts:

1. Fairness in monopoly capitalism has nothing to do with it. There is no free market system in place. The crash, bailout and subsequent desperate straits to date in the United States should have been lesson enough.

2. All the socialists and communists from Marx to Lenin to Mao have said that capitalism is at its root IRRATIONAL, which is the main reason they claim it can’t work.

Will the Valemax fleet harm the Chinese shipowners?

My recollection is that the majority, or at least the plurality, of iron ore carriers delivering to China were not Chinese. In other words, the Valemax plan would not eat into the Chinese shipping interests’ top or bottom lines since these international iron ore shipments weren’t on their books in the first place.

I agree with the CSA on one point.

Thirty five Valemax ships are altogether too much at this time. The current glut of capacity serves to drive prices down causing a lot of pain. If Vale could get out of those contracts I dare say they would. During the boom period prior to the bust in September 2008, shipping companies couldn’t order ships fast enough. Given the leasing market, every day without more capacity was millions unearned. The average day rate for a capesize vessel in 2007 was $116,000.00; the same rates during the first 9 months of 2008 topped out at $234,000.00 per day. The Australian port delays alone would mean two or three million dollars to a dry bulk company. What they didn’t figure on was the intersection of events: the bottom fell out of the market and it takes a long time to build these vessels. In other words, by the time they’d be taking delivery the market upon which those investments were based was no more.

Many shipping companies did in fact cancel orders reasoning that losing their deposits was less onerous than taking delivery and paying 100% of the price. Given all this, I would recommend that Vale use the CSA to lobby the Chinese ship builders to happily cancel the Valemax orders and return the deposits to Vale, all for the benefit of the Chinese fleet; no harm no foul.

At that time I will know that pigs fly and there is skiing in the 9th circle of hell.

Vale has a few ways to cut their losses. Per above, they are building hubs for the transport and storage of ore for the Asian market. Thus they can utilize the Valemax vessels even when they have no specific orders. The hubs also allow for the smoother and cheaper transfer of ore to smaller vessels should the destination require them. Vale is working at leasing the Valemax fleet to other companies which is another way to recover some of its over-investment.

Finally, the Chinese government has made it clear that its goal is to have 70% of its population in urban centers as soon as possible. That means more building than would be done, perhaps, in the entirety of Europe or South America during the parallel period. In other words, sooner or later, the Valemax fleet will be extremely profitable.

The position the CSA takes in helpfully suggesting the weaknesses of the Vale business model per hubs and real big ships is as generous as it is disingenuous. It well may be true that given current market conditions the current fleet is more than adequate to serve the transport of iron ore to China and elsewhere. I’d say that this is one rationale for building shipping hubs in Malaysia and the Philippines; it is a way to cut losses. Mr. Zhang’s concern with whether or not Vale can manage the ins and outs of the shipping business is moot. The company can hire specialists in that industry. Again I say that looking at the woeful record of China COSCO and all its incarnations, Mr. Zhang might want to stick to his knitting and petition the domestic shipping business.

Which brings me back to the above mentioned event.

With all the static coming from Mr. Zhang and his Association, why is a fully loaded Valemax bulker is now unloading its 388,000 tons at a Chinese port? This leads me to believe that what the CCP would call contradictions exist among the CSA’s interests and those of the government, ship builders, ports, infrastructure contractors, and steel corporations. Whether or not Vale can manage its Valemax scheme is an issue. Regardless of what it does, I predict that Mr. Zhang will ultimately be asked to be quiet.

Mark Weiss is an East Asian Studies graduate from the University of Wisconsin in Madison and trades stocks, bonds and precious metals. In this context he has been studying the Asian iron ore trade along with related industries: Dry bulk shipping, coal, Australian, Brazilian and South African mining, mining logistics, and primary Asian steel corporations.

by Captain John Konrad V (gCaptain) The stock of China Merchants Energy Shipping (CMSE – SHA) climbed higher after the release of the company’s latest investor report where the company announced that...

What is the definition of misery? Answer: Seasickness One of the first questions I get asked when a landlubber finds out I work at sea is, “Do you get seasick?” In...

Containerization is the reason we have a thriving global marketplace, but where did it all begin? The idea of it was actually conjured up on a busy dock in Hoboken,...

May 17, 2020

Total Views: 706

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 106,110 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 106,110 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club