FILE PHOTO: Evergreen Marine. Corp shipping containers sit stacked at the Port 2000 terminal in the Port of Le Havre, France March 14, 2017. REUTERS/Benoit Tessier/File Photo

By David Fickling (Bloomberg Gadfly) — While wedding bells have been ringing out across the global shipping industry, Taiwan’s biggest container line, Evergreen Marine Corp., has remained aloof.

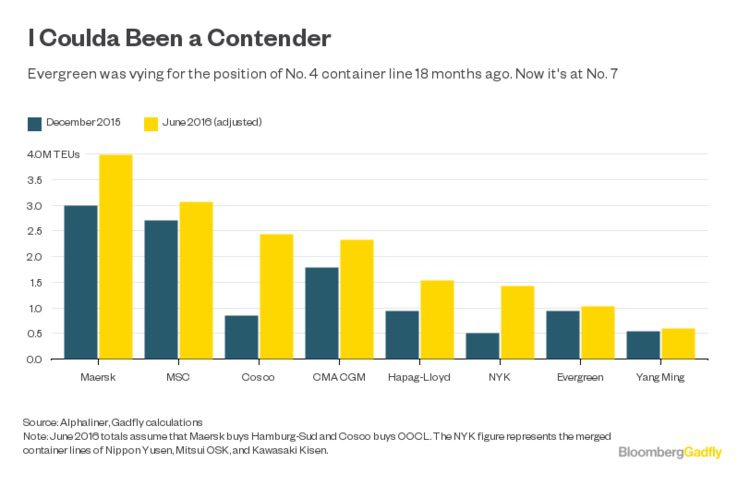

If mergers currently awaiting approval go ahead, the market share of the top five container lines will rise to 60 percent, from about 49 percent 18 months ago. With the last of the big marriages imminent, Evergreen looks like it’s being left at the altar.

State-owned Cosco Shipping Holdings Co. plans to buy Hong Kong’s Orient Overseas Container Line Co., or OOCL, for at least $4 billion in a deal that could be reached as early as July, the Wall Street Journal reported Wednesday, citing people it didn’t identify.

Such a transaction would hardly be a surprise: While a spokesperson for OOCL said the company wasn’t aware of a bid, Gadfly was predicting it six months ago. Still, this would cement a stark reversal of fortunes for Greater China’s shipping lines.

When the current round of M&A was kicked off last December with CMA CGM SA’s takeover of Singapore’s Neptune Orient Lines Ltd., Evergreen was Asia’s biggest box carrier and was fighting Hapag-Lloyd AG for the title of fourth-biggest globally, with capacity of about 936,000 TEUs, or 20-foot equivalent units. It’s been overtaken by both Cosco and the merged group that comprises Japan’s three major container lines, and its 1 million TEUs are now sufficient to make it only the seventh-biggest worldwide.

Single life has its advantages, though. Cosco, Evergreen and OOCL are all members of the Ocean Alliance, a grouping that pools its ships and allows customers a greater range of destinations and frequency. As a result, Evergreen gets some of the scale and revenue advantages of a formal merger without requiring a full-blown commitment.

There are other pluses. The entire shipping industry has benefited from the fashion for M&A over the past 18 months or so. Drewry’s weighted average of east-west container freight rates has risen 44 percent over the past year, to $1,464 from $1,020 per 40-foot box. Price volatility has dropped, too, as consolidating groups got a better handle on supply and demand.

Drewry gauge of east-west container rates, 12 months: +44%

Only the companies actually doing the deals have paid for this improvement, though. Evergreen’s NT$43.1 billion ($1.4 billion) net debt load — about 80 percent of the value of its equity — means it would probably have struggled to afford OOCL’s dowry. The debt may also have saved the company from a government-brokered shotgun marriage with Taiwan’s other big shipping line, Yang Ming Marine Transport Corp., which has failed to make more than a peppercorn profit since 2010 and has net debt at an eye-watering 482 percent of equity.

When the dust has settled on the container-shipping industry, Evergreen may have lost market share but it will remain a major player, and will have spared itself an expensive shopping spree. Wedding bells are all very well, but there are perks to being a wallflower.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

© 2017 Bloomberg L.P

Editorial Standards · Corrections · About gCaptain

This article contains reporting from Bloomberg, published under license.

Join The Club

Join The Club