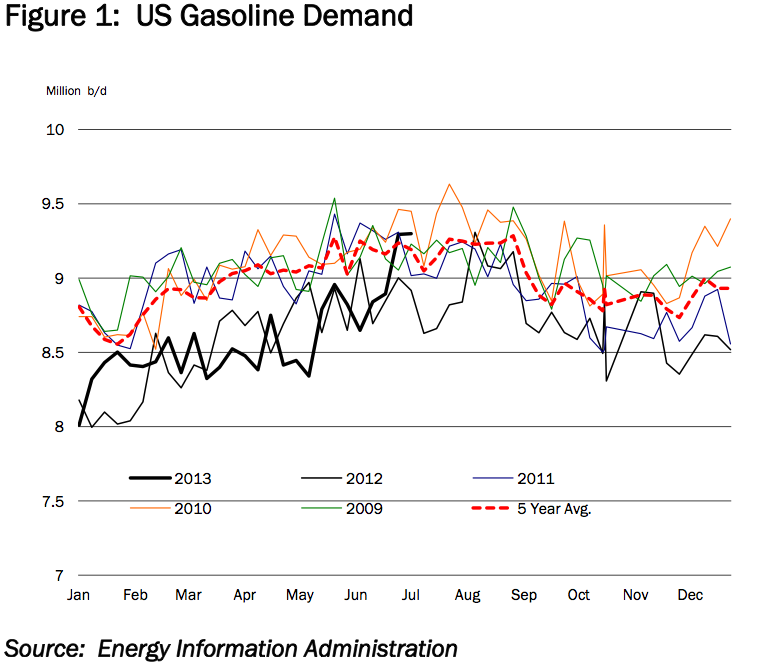

The current heat wave on both US coasts makes the idea of going anywhere, with the exception of the beach, an unappealing task. Nevertheless, roads and highways are crowded, which can be somewhat attributed to a slow but gradually improving US economy. As a result, there has been a recognizable boost in gasoline demand. Data from the US Energy Information Administration (EIA) shows that US gasoline consumption has remained above the 8.5 million b/d mark since the middle of May with the upward trend highlighted in Figure 1.

This uptick has catapulted US gasoline demand back to the seasonal heights of years prior. While part of this uptick can be explained by seasonality, the improving macroeconomic situation is also supporting this trend.

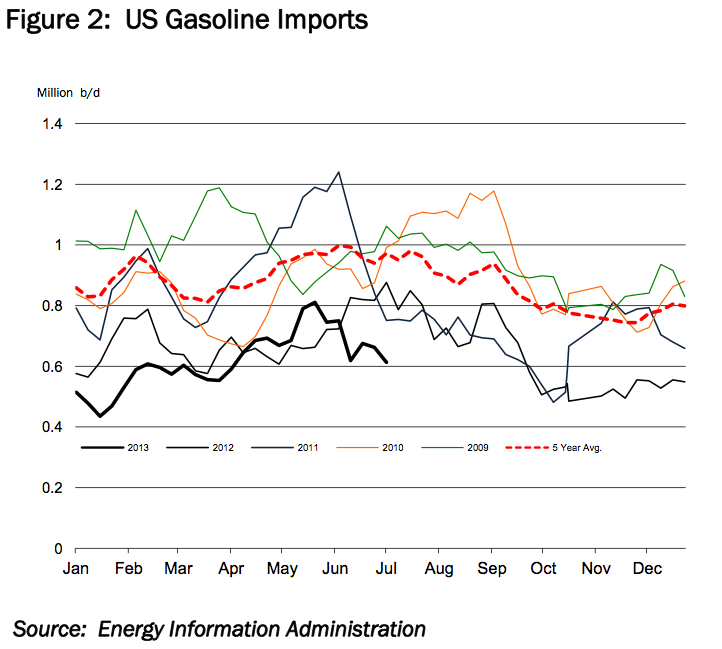

These improvements in demand have yet to translate into elevated seaborne import requirements.

Given Europe’s traditional surplus of gasoline, trade flows to the Atlantic Coast have historically been robust. However, data from the EIA shows that imports are hovering at the lowest seasonal level in at least five years and have dropped sharply since mid-May (Figure 2).

Part of this phenomenon can be attributed to Americans using more fuel efficient vehicles and government renewable fuel blending mandates. The other influence on reduced import requirements can be chalked up to rising utilization of domestic refineries. Since wrapping up a period of deep refinery maintenance in Q1, that took roughly 1.1 million b/d offline, refiners have increased throughput rates to three consecutive year-to-date weekly highs, with the most recent data at 92.4% of capacity (EIA). This has been pronounced in the USG, the nation’s refining hub, but refiners in the middle of the country are also keeping run rates elevated at 91.7% of capacity. This is being driven by their access to discounted crude oil that is produced in North Dakota and Canada. Available product volumes are set to increase further with the recent startup of a new central distillation unit at BP’s 413,000 b/d Whiting refinery at the start of July.

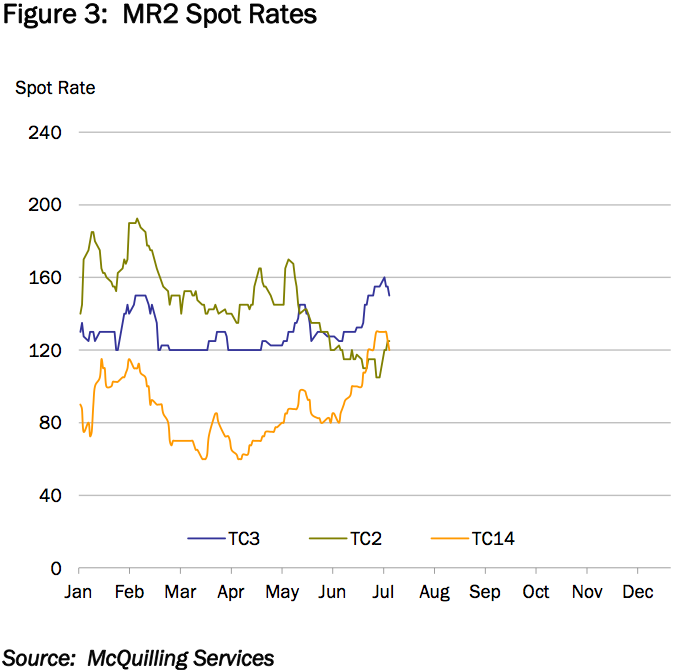

As a result of the higher refinery throughput rates, gasoline inventories are at 221 million barrels, the highest seasonal level in at least five years. These ample supplies have sapped the momentum of clean tanker rates from Europe to the US since the start of the year. On TC2, UKC to the US Atlantic Coast, rates have declined roughly 70 WS points from WS 190 in February (Figure 3).

There has been some upward pressure in the Caribbean market since the start of July, but this was primarily the result of elevated demand prior to the US holiday weekend and has recently started to retreat.

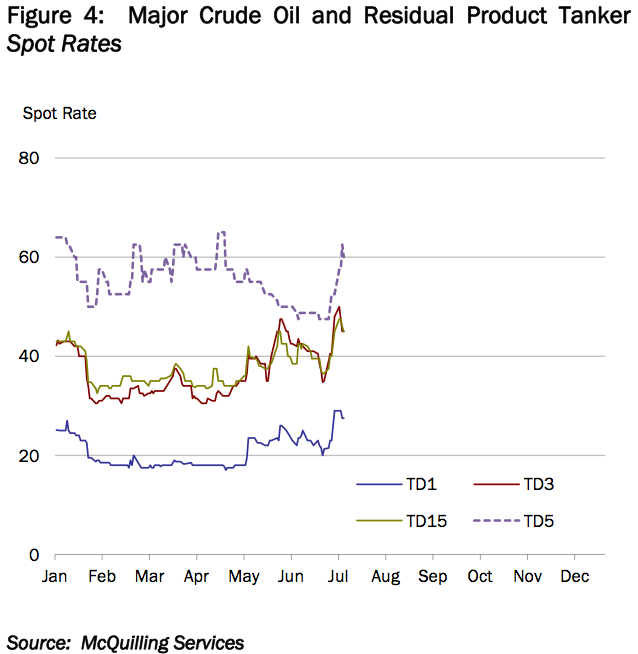

The backhaul earnings for USG exports to Europe (TC 14) have been climbing since April, supported by robust light and middle distillate cargo availability combined with European refiners operating at reduced capacity. Vessel availability has also been absorbed by exports to other destinations such as the Caribbean, South America and Africa. The advantage that US refiners have over their European counterparts is gradually being eroded through increased rail and pipeline delivery capacity to coastal regions. The spread between WTI/Dated Brent has recently contracted to below US $3 per barrel, compared to US $20 per barrel at the start of March. This could reduce the volume of petroleum products that are available for export if refinery utilization rates are scaled back due to falling margins. However if the spread stays in this range, West African cargoes should become more appealing to US refiners, potentially increasing seaborne import volumes. In the broader scope, this could provide a further impetus of the upward trend in dirty spot rates (Figure 4).

Additional pressure on US product exports to Europe could also arise from Russia. Since the start of summer some 770,000 b/d of Russian refining capacity returned from maintenance. Data from JBC Energy shows that refinery throughput volumes climbed to 5.7 million b/d in June, which was the highest monthly average on record. On the back of the country’s downstream upgrades, the output of high valued products such as ULSD is rising. Data from pipeline operator Transnefteprodukt indicates that ULSD exports from Primorsk, will be sustained at 810,000 tons over the next three months. These volumes are almost certain to compete with US seaborne exports.

In the coming weeks, the impact of the narrowing crude spread on US refinery operations and import volumes will become more apparent. If product demand and export opportunities remain robust, this could help alleviate pressure from mounting on margins. Increasing competition from other refining regions could reduce available outlets and will put even more focus on the economic recovery in the US and a subsequent rise in demand. Although the belief in this recovery appears to be gaining momentum, tanker market participants should keep in mind that life is not always a beach.

Updated: July 30, 2013 (Originally published July 11, 2013)

Editorial Standards · Corrections · About gCaptain

Join The Club

Join The Club