At the Marine Money Conference in New York City two weeks ago, Dr. David Zervos, Managing Director and Chief Market Strategist at Jefferies & Company gave a very interesting speech that helped to explain, from a macro-perspective, the issues that not only affect the financial crisis within the shipping industry, but that of Europe and the United States. The following is his speech:

In many ways as an economist, I’ve always sort of shunned one part of what people like yourselves might look to economists to do and that is to stand up in front of you and tell you where GDP growth is going. In a way I’ve always said there’s no reason why a couple of guys in ivory towers with 300-equation models of the global economy are going to be any better than anyone else in forecasting where the global economy is going.

In fact, they are probably some of the worst in forecasting where the global economy is going.

I’ve always said that when I want to try and get some idea of where global growth is headed in real terms, not inflation-generated growth, but real technological advance, real entrepreneurial behavior, real productivity gains, I want to be in places like this. I want to be talking to people on the ground in a shipping conference, in Silicon Valley, in the manufacturing plants of Asia and the like, or outside of Boston in the healthcare industry. So I hope that gives you some perspective of how I step back and think about the global macro views.

There are few things that I’d like to discuss with you today, and I would really like to leave it open for questions. One of my favorite parts of doing this is getting questions at the end and taking the discussion in the direction that the audience wants to go. I know you’re very focused on shipping and industry, and I’m going to try and pull you out of that in the next 40 minutes and get you to think about the bigger issues which I think have a big impact on all industries. I think they start with what’s going on with our policy-makers.

Something has fundamentally changed in most industries over the last 4 years, and that is a respect, or healthy fear of what happens on the macro side. Prior to that, I think many industries felt that they were generally insulated, stock traders could stock pick inside of various industries and say this balance sheet is better than that balance sheet, and they had a pair trade on where this one person would win and the other one would lose, and they were not about the tsunamis that would happen when everyone loses.

And I think that’s a good thing. I think we should all have a healthy respect for the bigger picture of macro economic trends and the dislocations and imbalances that can take place in the course of the way our markets are set up.

I’m going to give you five minutes on 2008 to the present, and I’m not going to go through everything on the slide deck here.

We have two major crisis that we’re fighting through, and they both come from the same thing. They both come from banks lending money to people who can never pay it back. It’s a pretty simple problem and it happens a lot. You ask yourself, “Why do banks do that”, and you can trace it back to usually some sort of regulatory arbitrage that says, “hey, if I make this loan, and I collect a big spread for a little while, I don’t really care if the guy doesn’t pay me back, because all I care about is two, three, four years of leveraged spread collection.”

In the US we lent money to subprime households. We took 5000 loans to people who were very unlikely to pay those loans back. We put them in a blender, we spun them up and out popped 60 to 70 percent AAA assets. Banks bought those with big spreads, 200 base point spreads in the beginning and they levered them. And they levered them because they didn’t need to hold any capital against it.

It’s a AAA asset.

So miraculously, there was an innovation. This innovation came along and we walked into banks and said “hey, here’s a piece of paper that’s AAA, doesn’t hold any capital, it yields LIBOR+200, how many can I make you?”

And the answer was, “Infinity. Please make more, go lend money to people who can never pay it back.”

And a lot of people made a lot of money doing that for many years. And some of them walked away. Some of the got caught holding the bag in the end when it was clear that none of these loans could be paid off.

There was a regulatory arbitrage. These assets were never AAA, they never should have been zero-risk weight, and there should have been a lot of capital held against the loan. But the fact is, we have a hole. Maybe it’s a trillion dollars, maybe a trillion and a half, or maybe just 500 billion dollars. But we have a hole, and we haven’t realized all these losses yet and a large part of what we’re doing is trying to figure out a way to realize those losses, distribute those losses, and get on with life without creating a huge disruption in the US or the Global world economy.

In Europe, they didn’t lend to sub-prime households, they lent to sub-prime countries. Slightly different.

In 1999, a country like Greece, which spent the better part of a 150 years prior to 1999 in default on its sovereign debt. So from the 1821-1826 time frame when Greece was first given independence from the Ottoman Empire they started issuing debt to finance a war, they went into default on that, then there were a series of defaults all the way through the late 1800s, into the early 1900s, WWI, WWII.

50 percent of the time they were in default over that period.

Miraculously, in 1999, through some beautiful accounting tricks, they made it into the EU and their debt was deemed zero risk weight assets on European Bank balance sheets. They were the equivalent of a German bond.

Again another fantastic arbitrage opportunity for the banks. Big spread, triple-A, no capital.

“Hey, how many Greek bonds would you like?” And we waved them in.

Then we waved in Irish bonds, and we waved in Portuguese bonds, and lots of other bonds and there were huge booms in these countries because they had the cheapest interest rates they had ever seen, just like we saw huge booms in the housing business in the US, and of course it was all on this toxic debt that somebody was getting paid a lot of money for owning in a very short period of time, but in the end somebody else was getting left holding the bag. In the US it was us taxpayers with our FDIC insurance that we supply to our banking industry, and in Europe, they still haven’t figured out who is going to pay for the bill. They are fighting that one out as we speak.

They don’t have an FDIC. They have 17 FDICs, they have 17 central banks, they have 17 treasuries, 17 different tax bases, and they are all fighting every day to pin it on somebody else. And that is what you see throughout most of the political shenanigans going on as we try to realize losses in the Spanish market, in the Greek market, and the Irish market, and the like.

The point is, we have these losses.

We lent the money and if we allow this debt to be overhung on the global economy, particularly in the US and Europe, and at the same time we don’t inflate that debt away or write that debt off, we will create a 1930s outcome.

If there’s one thing that economists have learned, and I think Ben Bernanke holds nearest and dearest to his heart at the Federal Reserve, is that if you take a hold bunch of debt and mix it with a whole bunch of inflation, you will destroy an economy. Because the value of that debt keeps going up in real goods and services terms. So part of the fight here is to take that debt and figure out a way to get rid of it in the most effective way. And we’ve seen an attempt to write the debt off, and to just create losses. That was the PSI in the Greek bond market… and that didn’t go so well.

That was a pretty messy, complicated, legal experiment. We’ve seen write-offs of debt in Argentina before, and to this day we’re still having court cases of who’s going to get paid and who doesn’t get paid.

The age-old way of getting rid of debt is sort of why central banks were invented in the first place. To print money. Inflation. Inflation gets rid of debt, inflation devalues the real value of that debt.

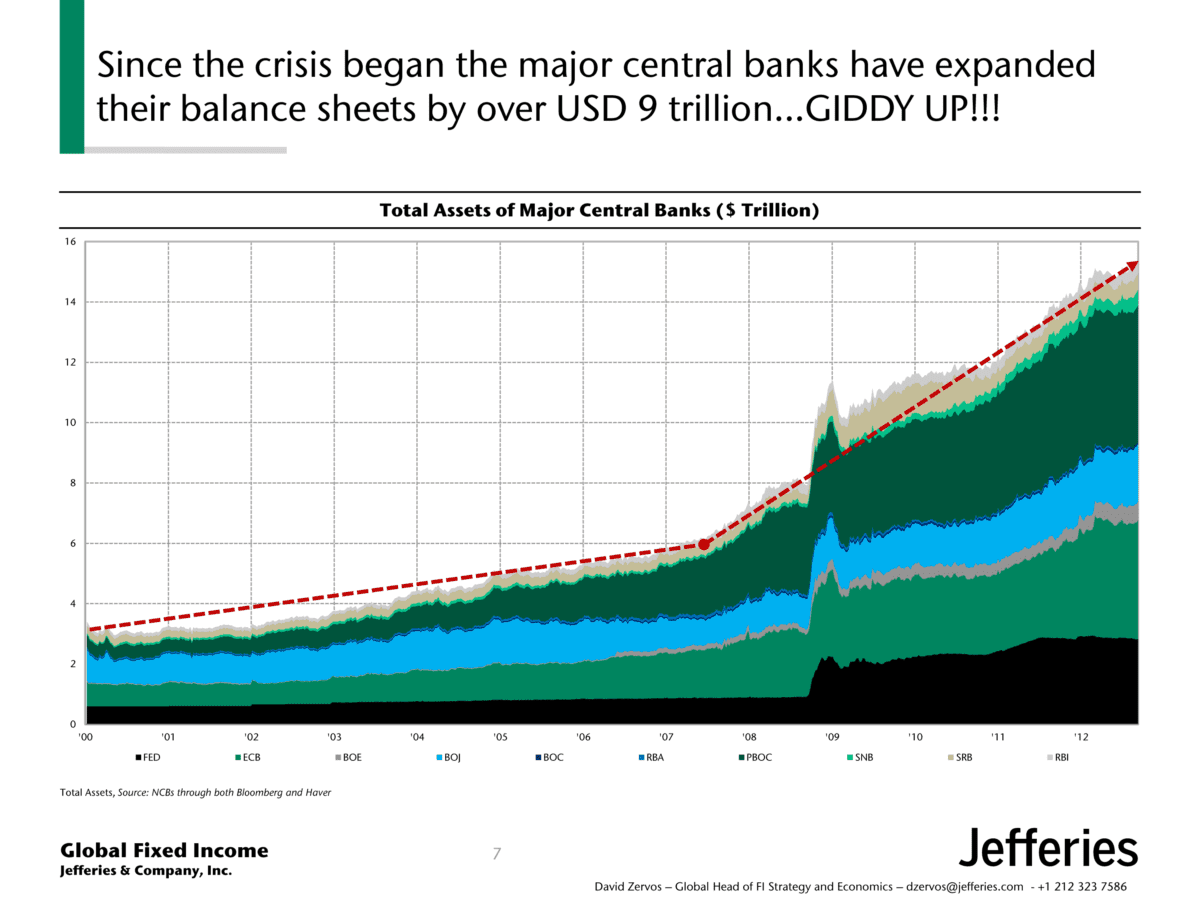

This is one of my favorite charts in the entire global macro economic world I live in. This chart shows you the total assets of the major central banks in the world.

click for larger

These are balance sheets, these are assets physically on the balance sheets. You can see that as our crisis began in the middle of 2007/2008, assets on central banks were $6 trillion up from 3 trillion in the beginning of the decade. So they doubled the size of their balance sheets in about 7.5 to 8 years. Now we’ve gone from $6 to a little over $15 trillion worth of assets.

These guys have bought $9 trillion worth of stuff. $9 trillion, in the better part of 4.5 years.

New program guys. Take note. $9 trillion. This is not the same set of central banks you had to deal with during most of your career.

Source: National Central Banks balance sheets and GDP figures, click for larger

Now, where does the central bank get the money or financing to buy assets? How do these guys come up with $9 trillion worth of stuff? Do they come to the marketplace and say “hey, I have debt issue for you, issued by the Fed or BOJ, here’s some debt I’d like to you buy it. And then I’m going to go out and buy some other stuff.”

That’s how Jefferies would finance an increase in their balance sheet. Or how any investor here would finance an increase in their balance sheet. They would go to the markets and raise capital.

Central banks don’t have to do that. Central banks have one of the greatest advantages known to man when it comes to investing in markets. They get to issue debt. That debt has no coupon, and it never matures. That debt sits in your back pocket, buys you lunch. That debt is money. That is the debt of a central bank.

They print their own debt.

Beautiful. I wish I could do that. I wish anyone who ran a business could do that, but we can’t, we have constraints. They don’t. They have a monopoly on the printing of money.

And guess what… they used it pretty aggressively to fight the de-leveraging and dis-inflationary forces associated with these massive losses that exist in the US and European capital markets. That’s what they are fighting.

Now, most of you took an economics class at some time in your life, I hope. Or you wouldn’t be in the business world. And there was this famous economist named Milton Friedman who said probably one of the most profound things any economist has ever said.

“Inflation is always and everywhere a monetary phenomenon.”

Now I just put a chart up there that shows you that we printed $9 trillion worth of global money in 4 and a bit years. Milton Friedman would look at that chart and tell us there’s going to be some inflation. Might not come today, might not come tomorrow, it might not even coming in two to three years, but what we are doing with our central banks is that we are diluting the value of cash.

That’s what we are doing.

In a way, it’s the right thing to do. The alternative to this is to watch massive defaults run through the system. To watch unemployment rates run to 25 percent. To watch house prices fall another 30, 40 or 50 percent. To allow the debt losses to be realized, businesses to go bankrupt, economies to go into depression, and then rise out of that from a much lower level of wealth, and a much lower level of income.

That was the solution to our debt problems in the 1930s. It wasn’t a great solution.

The solution to some of our debt problems coming out of World War II was the 1970s. We inflated away a lot of our debts in the United States. And if I think about what we’re deciding on here, in the hallowed halls of the Central Bank at 20th and Constitution Avenue in Washington, DC, they are making an active choice to either choose a 1930s solution or a 1970s solution to solve our debt problem.

So then you have to ask yourself, as an investor, what do you do?

If I have every one of these central banks on the program. And by the way, the Bank of Japan has announced an inflation target for the first time in 20 years. The Swiss National Bank is seeing huge increases in its balance sheet and in fact is the most active printer of money in the market today. That in itself tells you all you need to know, if the Swiss are doing it, everyone’s going to do it.

The Japanese have been trying this for a while, but have been really slow. They are going to come around next year and one of our bigger themes is that with the new government in Japan in 2013, you’re going to see a BOJ that looks a lot more like the central banks of the rest of the world. So keep your eyes on the Nikkei and the Yen. There’s going to be a little bit of catch-up there and we think that’s one of our better trades for 2013.

But, importantly, going back to our original chart, how to do you think about investing in a world where the central banks are diluting the value of cash?

If your asset in the beginning of 2011 was a bank deposit earning zero, by the end of 2011, after the headline CPI was at 3 percent for the year, you lost 3 percent of your real purchasing power sitting in the bank. You could buy 3% less goods and services.

This year, the headline CPI year-to-date has been 2.2 percent, so you lost another 2.25, by years end might be 2.5 percent. Sitting there, earning zero, losing in real terms. These guys are making it very hard for anyone to sit around and take no risk.

This is their goal.

Their goal is to try and get the global economy jumpstarted. It’s actually a noble goal, and it might end in tears, and it might end fantastically, we don’t know. But it’s certainly a lot better than sitting there with all of us holding cash and taking no risk, and having no innovation, and no entrepreneurial behavior, and no productivity gains.

What Ben Bernanke refers to in his speeches is a portfolio imbalance channel is the channel by which they are trying to drive real growth in the global economy. They are making it very expensive for people to sit in cash, and cash-equivalent assets. That’s their goal.

If you think back to the 1930s and what they are trying to avoid at all costs. What Cains wrote about back then was animal spirits. Now animal spirits can drive bubbles up and they can drive bubbles down. What came in the 30s were negative animal spirits. Negative reinforcing animal spirits. When you lose 30 to 40 percent of the value of your house, when your stock portfolio drops 30 to 40 percent, when the value of your ship drops 50 percent, and the income from your ship starts to go down, your first inclination isn’t to go out and take more risk.

“Hey, let’s build another ship!”

No. You inclination is to sit in a corner, hold on tight, wait for the tornado to go by and hope you still have a roof on your head when it’s all done. But if everybody does that, we will have no real growth. If nobody is willing to take risk, nobody wants to go out and invest. We will have a great depression. There is no upside. Everybody just hoardes. That was the 1930s.

This is almost the equivalent of an anti-hoarding law which was put in place in the 1930s. “I’m going to make it expensive for you to sit there and do nothing.”

That’s what the central banks have said. “I want you taking risk, I am going to drive people out of cash and cash equivalents, make it too expensive to sit there, drive inflation higher, and ultimately get (hopefully) some real returns on some real investments. And some real productivity and technological change.”

Ultimately the business cycle isn’t dead.

That’s the goal, that’s the idea, that’s what we’re all after.

In the end, we may not get that real growth, but we will get a lot of nominal growth. We will get money printing, we will get inflation, if we don’t get real growth. And that nominal growth will go a long way to devaluing our debts and our deficits. The debt to GDP ratio will go down, as long as the denominator goes up faster than the numerator, which means as long as nominal income grows faster than nominal debt.

That is the goal of all of these policies. Get rid of those bad debts. Hopefully we can do it through real innovation, if not we’re going to use the printing press. So as an investor, you have a choice of assets. I’d like to take two different kinds of assets. Assets that the central bank can dilute, and assets that the central bank can’t dilute. I call them printable and non-printable assets. You can have all your wealth in cash and T bills and tomorrow, the central bank can turn around and go, “Hey, I’m going to double the amount of money in the system.” And the value of your cash and your T bill will go down by about 50 percent. You’ll be able to buy 50 percent less stuff.

Then there’s assets that the central bank can’t print. This beautiful hotel building, the Plaza Hotel. Can the Fed print a Plaza Hotel? No. It’s a hard asset.

In the end, when you think about printable and non-printable assets, and a set of central banks that are doing this, your only hope as an investor for wealth preservation and for capital appreciation will be to get out of the way of the big train that’s coming and diluting the value of cash.

That is their chosen path.

And the people who are going to pay the bill for all of the bad lending are the people who will allow themselves to be called financially-repressed. Those who will sit there and earn nothing in the face of higher inflation. And by the way, this happened in the past in the United States. In the 1940s during World War II, the treasury market was manipulated by the government and the 10 year note yield was capped at basically 2 percent.

The average inflation rate over the 1940s was 6 percent. So in the beginning of the 40s until the end of the 40s, you lost 4 percent real, every year. You were financially repressed. You helped pay for the war.

Now we used to have big posters on the wall back then that said “Fight or buy bonds” with Lady Liberty pointing at you. And people did that out of patriotism. Not clear we’ll have a lot of patriots who want to step up now and lose 4 percent per year to help save a bunch of subprime borrowers in Europe and in the US. So we might have a few other solutions to go through.

The point is, as I go around talking to investors about how they should structure their global portfolios, I operate with one big picture theme, and that is, you have to avoid printable assets. You have to avoid assets that get diluted by what these global central banks are doing. And if you take one thing away from my talk today, I hope it’s that.

I’m going to talk for another 8 minutes on a few other issues that I think are important for you guys, and then I’m going to open it up for questions. One is the fiscal cliff, and the other is an outlook for Europe into next year. There’s a chart on the fiscal cliff that I’m going to put up so you guys know where we are in the discussion. This little pie chart.

click for larger

Bush tax cuts, AMT, payroll tax cuts, non defense spending, defense spending and the dividend tax rate. This is a $600 billion potential hit to the US economy. That amounts to about 3.7 percent of GDP. So, folks who talk about the fiscal cliff get very hot and bothered because we go from an economy that’s growing from 1.5 to 2 percent, to one that is shrinking by 1.5 to 2 percent. And that’s a pretty different world for all of us. So it’s a real risk. And there’s a real risk that we’re going to have a very significant change in how our tax policy operates in the United States. I don’t think anyone denies that. The election would suggest that we’re going to have a more progressive tax structure, and maybe it’s not a bad thing. Maybe it is a bad thing. It’s hard to know.

We’ve spent our time in the US economy with 70 percent marginal tax rates, 90 percent marginal tax rates. 30 percent marginal tax rates at the top end. We’ve had a lot of different experiences, and by and large, every decade with an exception of a few which didn’t have much to do with tax policy, we’ve grown at a reasonable rate. Some decades better than others, but it’s very hard to correlate tax policy to growth. We had very high taxes in the 60s and 70s and they were very high growth periods.

So, my point is, it is a big deal. We’re supposed to watch it, we’re suppose to be nervous about it, but at the end of the day, looking at the fiscal cliff in isolation is silly. We have the most activist central bank in probably the history of the United States and they have what they call a “dual mandate.” Price stability and full employment. If you see this materialize in January, there will be an equal and opposite reaction coming from monetary policy to try and stop every bit of that drag on global growth and US growth. They will throw lower interest on excess reserves, funding for lending programs, more mortgage purchases, faster balance sheet expansion, more money printing, more driving of people into risk assets, more risk taking. We might not get real growth, but we’ll definitely get nominal growth.

And I think, at the end of the day, that’s our caveat to the whole fiscal cliff. If you drive equity prices up 10 percent, you create $1.5 trillion worth of wealth in the US economy to fight that $600 billion worth of drag. You drive interest rates down another 50 base points in the private sector credit markets, you create another $100 to $150 billion worth of savings, annually, in interest costs.

That’s what they’ll do.

So there’s a lot of counter balancing to this fiscal cliff. You don’t hear about it on CNBC or Bloomberg, because a lot of people like the doom story. People like to get on there and go, “this is the end of the world, it’s a $600 billion hit.” Doom sells.

But there’s a backstop, there’s a parachute when we go over the cliff, and it’s Ben (Bernanke), and he pulls the ripcord really hard.

I’m going to talk a little about Europe.

Our views at Jefferies in Europe have evolved quite a lot over the three years I have been here. I started my career as a European bond strategist in 1993 in London. So I watched the EU happen from the ground and when I left in 2000 after it all came together, I left with my tail between my legs shaking my head never understanding why in the world these people wanted to do this. And to this day, I’m still a die-hard Euro skeptic.

That said, it’s a political project, not an economic project and we have to understand, and as an American, I don’t understand it, but we have to understand that there’s this desire to be European, and they are willing to pay a really big price for that nomenclature.

In the end, I think what we learned in the crisis is that this is going to be nearly impossible to break down. The ECB structure is such that when the banking system of a weak country sees deposit flight, the deposits go to the strong country. Suffice to say, money leaves one country and goes to another country, but it recycles itself back to the ECB. So, while there’s no money left in Greek banks from depositors, the money went to Commerce Bank or Deutsche Bank. Deutsche Bank then puts the money on deposit at the ECB, then lends it back to the Greek Bank. So the Greek Bank still has the Euros, but now it’s a loan from the ECB. And Deutsche Bank is now a creditor to the ECB. But Deutsche Bank is really a creditor through the ECB as an intermediary back to a Greek Bank. So at the end of the day, all of this chaos has produced a huge credit from the German and the Dutch banking systems back to the ECB to fund peripheral banking systems. And Germany is on the hook for something like 700 billion euros.

That’s a lot of dough in a $2.3 or $2.4 trillion economy. You’re talking nearly 30 percent of GDP. That’s not to mention all the other exposures through government bonds and the like. In the end, you could have said before all this happened maybe it’s best for Germany to walk away from all of this. Why stick around and help these people when you can get out? But the structure of the ECB has actually mutualized the debt. Germany never signed up for mutual debt, and you hear a lot about euro bonds and the issuance of European mutual debt and the like. It already happened through the ECB, through the back door.

They’re in. They’re stuck. They’ve already mutualized this debt.

And if you come to that conclusion, that there is no exit for the guys who have lent the money back to the ECB, then, you realize this thing has to go in a way that is together and not apart because the pain process of unwinding that for the strongest nations is just too high.

That doesn’t mean Greece can’t exit.

Greece could exit in a managed way. You still have all the policies that Mario Draghi has put in place with the OMT structure to backstop the other nations. There may be a political reason to want to go after the one rogue nation that violated all the rules and should have never been given that money.

I’m sympathetic to that view.

I’m also sympathetic to the view that a country like Finland, which hasn’t had a bunch of people come in and pile into its banking system and doesn’t have a lot of credits to the ECB and say, “You know what, I don’t want to be a part of this thing, I like Sweden, I like Norway, they’re not a part of this thing, life is good up here. I’m out.”

So we could have a smaller EMU. We could have more mutualization of debt, because it has already implicitly happened, and we could see some form of a Euro bond, some form of a unified fiscal policy develop in Europe whereby they try another way to keep countries from abusing the privilege of being in the club and issuing debt as if they were Germany when they were really Greece.

There’s a possibility of that.

It looks like the enforcement mechanism might just be the ECB, the ECB through its OMT program is targeting monetary policy based on people signing Memorandum of Understandings and keeping their fiscal house in order. That may be the way to go. It’s not clear, but one of the most important things to remember now is the ECB balance sheet, and Mario Draghi, are backstopping this project. And as long as the guys who print the money are willing to write the check, we don’t have to worry about the systemic consequences of a complete breakdown in Europe. Up until the summer, I think a lot of us thought there was a reason to worry about this, I think that card is off the table for now. It doesn’t mean it’s off the table forever, but I think it’s off for now.

We are going to go for a more Lira-type Europe as opposed to a Deutsche Mark-like euro. We’re going to have an Italian running the show at the ECB, the Germans are going to accept higher inflation, because they have no choice, and we’re going to end up doing what Ben Bernanke is doing here, which is probably a little too much inflation over the long run, it gets rid of some of the debts, and transfers wealth from Germany, who’s a creditor nation, to the south, who is a debtor nation, because inflation is really just a tax on creditors.

That’s the end game.

How that gets done politically remains up in the air, but the bottom line is that’s the only equilibrium here because at this point, the northern creditors can’t leave. They’re stuck. They HAVE to realize the losses, and it’s just a question of keeping the politics together as those losses get realized.

One of the most important things to remember about these lending crisis, and I started by talking about lending money to people who could never pay it back, one of the most important parts about the realization process is that you’re never going to get the money back. The guy that lent the money is the guy who has to lose. We lent money to some kid to buy a $400,000 house outside Las Vegas when he should have been living in his mom’s basement. He’s now back in his mom’s basement and we’re never getting that $400,000 back. Somebody has to eat it, and that’s the guy with the wealth. That’s the creditor.

The German guy lent the money to the Greek guy. The Greek guy should never have had the money. He’s gonna take a loss.

This process of loss realization is what we’re going through right now. It’s kind of politically messier in Europe than it is here, but it’s the same process, and it’s going to be cushioned by a constant devaluation of all debts.

By Vince Golle (Bloomberg) Shipping costs are rising as hundreds of container ships that typically transit the key maritime artery of the Red Sea and Suez Canal are rerouting after a...

In the realm of economics, where numbers often paint a more eloquent picture than words, we sometimes find ourselves bamboozled by the outliers. Let’s talk about France and the latest...

By Esteban Duarte, Maria Elena Vizcaino and Natasha White (Bloomberg) –The world’s biggest ocean friendly debt swap is coming together in Ecuador, with Credit Suisse Group AG offering a yield of...

May 7, 2023

Total Views: 2329

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 104,523 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 104,523 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club