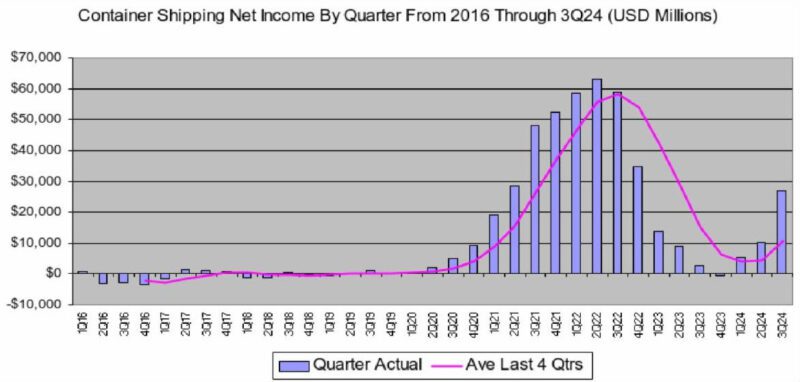

The container shipping industry has experienced a remarkable turnaround in the third quarter of 2024, with total net income soaring to $26.8 billion, marking a staggering 164% increase from the previous quarter, according to renowned industry analyst John McCown.

The impressive growth trend, which began in the first quarter of 2024, has been primarily fueled by capacity tightening in the Red Sea region and strong global demand.

In his Q3 financials report, McCown reports that compared to the same quarter last year, net income skyrocketed by 856%, representing a $24.0 billion increase. This dramatic upswing follows a period of declining earnings that lasted for six consecutive quarters after the industry’s peak earnings of $63.1 billion in Q2 2022.

Credit: John McCown

McCown attributes this financial resurgence to pricing dynamics. “Just as pricing drove those roller coaster results, it was the main driver in the recent quarters. The difference is that the catalyst for the latter was pricing increases emanating out of the Red Sea situation,” he writes. The Red Sea route, which accounts for approximately 25% of global container miles, has played a crucial role in shaping market conditions.

Despite the overall positive trend, McCown notes a widening dispersion in financial performance among carriers. While all eleven major companies reported higher net income compared to the previous year, eight experienced decreases when comparing the last twelve months to the prior period. European carriers, with their broader market exposure and less concentration on major east-west routes, showed the most significant variances.

McCown’s report also highlighted the resilience of global container volumes, with a 4.7% year-over-year increase in the third quarter of 2024. Although this represents a slight pullback from growth levels seen in Q1 and Q2, it marks the fourth-highest quarterly gain in over three years.

The industry’s recovery is further evidenced by the record-breaking worldwide loaded TEU (Twenty-foot Equivalent Unit) volume of 47,121,793 in Q3 2024, surpassing the previous high set during the peak of the pandemic by 2.1%.

Year-to-date figures for the first nine months of 2024 show a 6.3% increase in total volume over 2023, reaching 136,714,259 TEU – a figure that even surpasses the pandemic-era volumes of 2021 by 1.5%.

While Q3 2024 appears to mark a peak in this current cycle, ongoing geopolitical catalysts and market factors suggest that the industry’s financial landscape remains subject to rapid changes in the near term.

The conflict in the Middle East could significantly alter expectations of looming overcapacity in the container shipping sector. The prolonged Red Sea disruptions are absorbing vessel capacity and keep freight markets tighter than anticipated.

The Federal Maritime Commission says it is closely monitoring new surcharges being introduced by ocean carriers amid the escalating security crisis around the Strait of Hormuz, warning that emergency fees must still comply...

The effective closure of the Strait of Hormuz is now rippling through global container supply chains, with new data showing a dramatic surge in cargo diversions as carriers scramble to...

March 10, 2026

Total Views: 865

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 107,414 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 107,414 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club