U.S. container ports are anticipating a surge in volumes this month as retailers prepare for the holiday season amid concerns of a possible labor strike at East Coast and Gulf Coast ports.

“This is a critical time as retailers prepare for the all-important holiday season, and we need every port in the country working at full capacity,” said Jonathan Gold, Vice President for Supply Chain and Customs Policy at the National Retail Federation. He urged labor and management at the affected ports to negotiate in good faith to avoid potential disruptions.

The contract between the International Longshoremen’s Association and the United States Maritime Alliance, covering East and Gulf Coast ports, is set to expire on September 30. With the ILA threatening to strike if a new agreement isn’t reached, the NRF has called for both parties to come to terms before the deadline.

The outcome of these negotiations could have far-reaching implications for the holiday shopping season and the overall health of the U.S. economy.

Ben Hackett, Founder of Hackett Associates, noted that concerns about the potential strike have already impacted import levels. “This has caused some cargo owners to bring forward shipments, bumping up June-through-September imports,” Hackett explained.

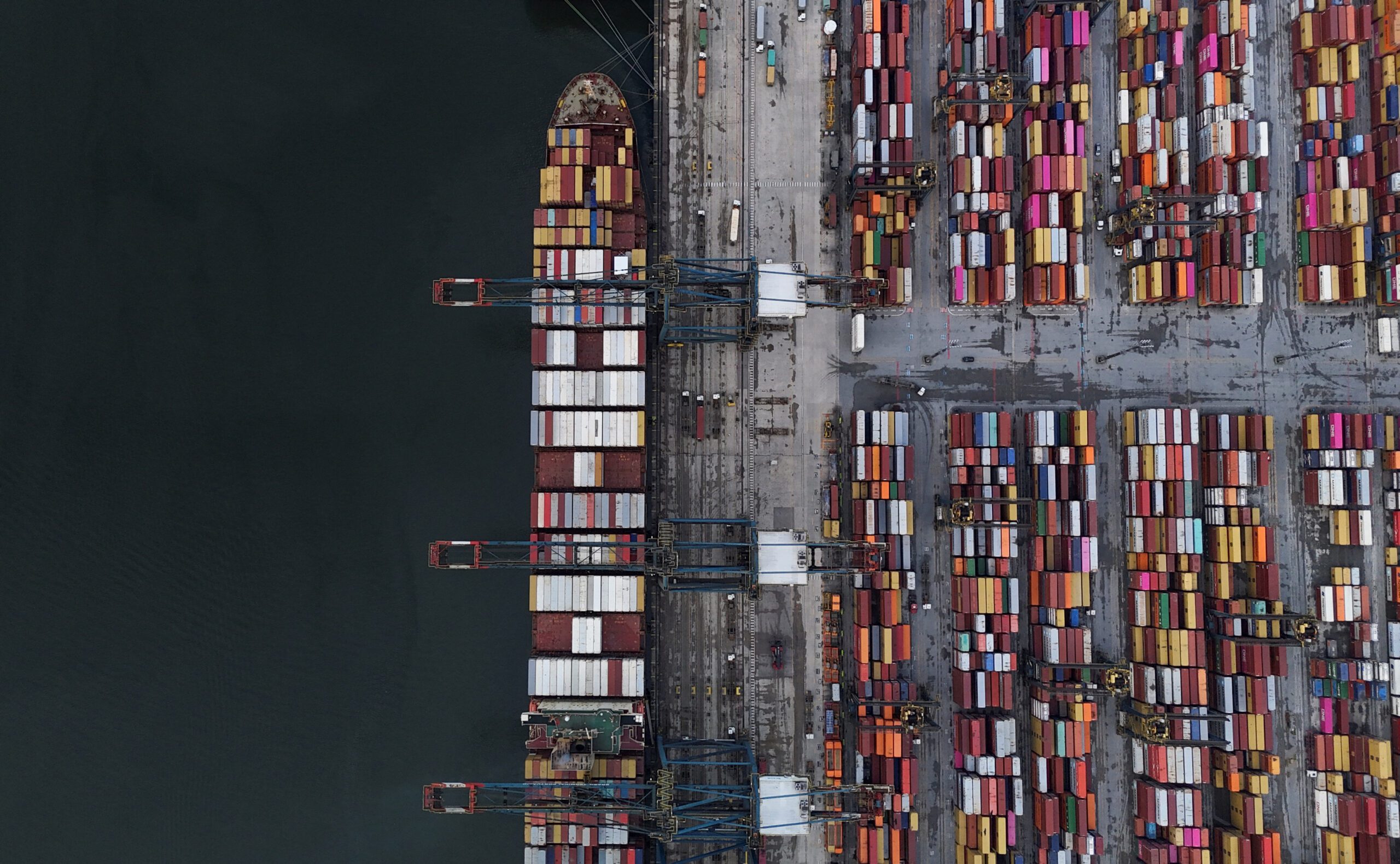

Despite these challenges, U.S. ports have seen record-breaking numbers, according to the NRF’s and Hackett Associates’ Global Port Tracker report. Notably, the first half of 2024 saw a significant rise, totaling 12.1 million TEU—a 14.8% increase compared to the same period in 2023.

In July, ports handled 2.32 million Twenty-Foot Equivalent Units (TEUs), up 21% year over year. September is forecast to see 2.31 million TEUs, a 14% increase from last year.

However, projected TEU volumes for the coming months show more modest growth: October at 2.08 million (up 1.3%), November at 1.92 million (up 1.6%), and December at 1.89 million (up 0.9%). These figures would bring the 2024 total to 24.98 million TEU, a 12.3% increase from 2023.

If the forecasts hold true, 2024 will see a seven-month period of import levels at or above 2 million TEU—the longest such stretch since the 19-month run through September 2022. Looking ahead, January 2025 is projected to handle 1.96 million TEU, a slight 0.3% decrease year over year.

The import figures coincide with NRF’s forecast for 2024 retail sales. Core retail—which excludes automobile dealers, gasoline stations, and restaurants—is projected to grow between 2.5% and 3.5% compared to 2023.

Editorial Standards · Corrections · About gCaptain

Join The Club

Join The Club