The latest edition of Drewry’s Global Container Terminal Operators Annual Review and Forecast has highlighted significant changes in the composition of Global Terminal Operators (GTOs) despite the total number of GTOs remaining constant at 21 in 2023.

New entrants Adani, AD Ports Group, and Hapag-Lloyd have reshaped rankings, while the acquisitions of SAAM Ports and Bolloré have led to their removal from the rankings.

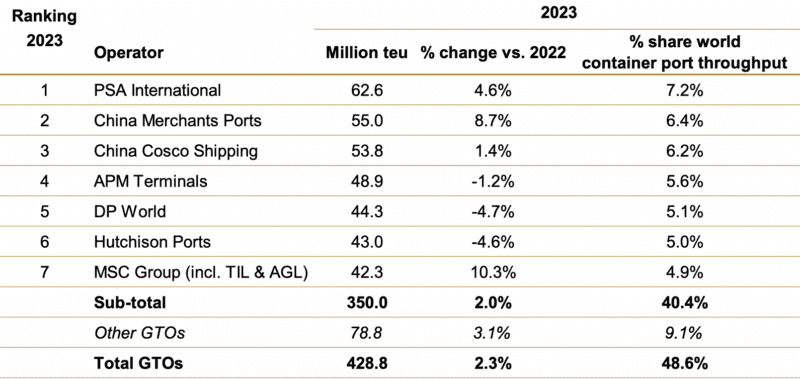

The top seven global terminal operators (GTOs) now handle over 40% of global port throughput on an equity-adjusted basis, with each reporting over 40 million TEUs in 2023. Despite smaller GTOs’ expansion efforts, a significant 30 million TEU gap persists between the leading operators and the rest, according to Drewry.

Leading global/international terminal operators, equity-adjusted throughput, 2023. Source: Drewry’s Global Container Terminal Operators Annual Review and Forecast 2024/25

PSA International maintained its top position with 62.6 mteu in 2023, while China Merchants ascended to second place with 55 mteu. MSC Group experienced the most significant growth, bolstered by its acquisition of Bolloré Africa Logistics, which led to a 10% increase in throughput. Adani entered the rankings at 13th place with 6.5 mteu, driven by growth in the Indian market, and is expected to rise further. AD Ports and Hapag-Lloyd are also poised for better rankings in 2024 following their 2023 acquisitions.

The overall annual growth in equity-adjusted throughput for the 21 GTOs was 2.3%, markedly higher than the global port handling increase of 0.3%.

However, revenue trends were mixed due to the normalization of congestion-related storage income to pre-Covid levels, offsetting gains from inflation-linked tariff increases. Still, the Drewry Global Container Terminal Revenue index rose in the last quarter, driven by strong US demand and congestion-related income from the Red Sea crisis.

“While congestion is starting to ease, the recovery of consumer demand in import-dominant markets will provide continued support to the average revenues reported by the GTOs that are included in the Index,” said Eleanor Hadland, author of the report.

Capital expenditure among sampled terminal operators reached $5.5 billion in 2023, a 9% increase from the previous year and the third consecutive annual rise. Investments focused on capacity expansion and equipment modernization, with five GTOs spending over $500 million and DPW and PSA each investing over $1 billion.

Sustainability has also become a critical focus for port and terminal operators, with decarbonization being the most pressing issue. Most of the 21 global operators aim for net zero by 2050, with Adani and A.P. Moller-Maersk targeting 2040, Hapag-Lloyd 2045, and Chinese operators aligning with a 2060 goal.

In a landmark deal announced on Tuesday, Hong Kong-based CK Hutchison will sell its 80% stake in Hutchison Ports Holding to a Blackrock-TiL consortium, positioning Mediterranean Shipping Company (MSC)—already the...

Key transhipment ports around the world are facing severe congestion in response to the Red Sea crisis, with Singapore being a prime example. The escalating crisis is due to abrupt...

Maritime industry consultancy Drewry flags potential challenges for the US East Coast ports due to the diversion of Baltimore’s container volumes combined with expected market growth in 2024. The Port...

March 29, 2024

Total Views: 2064

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 104,716 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 104,716 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club