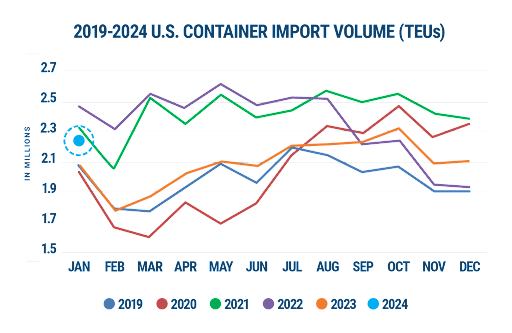

U.S. container import volume increased 7.9% in January 2024 from December 2023, marking the largest month-over-month growth for January in the last seven years, according to Descartes Systems Group’s (Nasdaq: DSGX) (TSX:DSG) latest Global Shipping Report.

This surge was primarily fueled by a 14.9% rise in imports from China, with the Ports of Los Angeles and Long Beach picking up the most volumes. As a result, the volume share at top West Coast ports increased significantly, accounting for 43.0% of the total import container volume – an increase of 3.3% from December 2023. In contrast, the top East and Gulf Coast ports saw their share decrease to 42.4%, down by 2.5%.

Compared to January 2023, last month’s imports were up 9.9%, and 9.6% higher than pre-pandemic January 2019.

Graph courtesy Descartes

The report also noted that ongoing issues such as Panama’s drought and the Middle East conflict have begun to affect transit times significantly, but not necessarily import volumes. Panama’s drought, in particular, has disrupted traffic through the Panama Canal, with the number of transit slots in January increasing slightly to 24, still well below the usual 36. Moreover, the conflict in the Middle East has affected traffic through the Suez Canal, leading to more ships opting to go around Africa’s Cape of Good Hope.

“January was another solid month driven by surprisingly strong imports from China,” said Chris Jones, EVP Industry and Services, Descartes. “The combined effect of the Panama drought and the conflict in the Middle East is beginning to impact transit times, particularly at the top East and Gulf coast ports.”

Descartes’ report also cautions about the potential for labor disruptions at South Atlantic and Gulf Coast ports. The contract between the International Longshoremen’s Association (ILA) and the United States Maritime Alliance (USMX) is due to expire in September 2024, and the ILA has indicated that it will not extend the current agreement and has advised members to prepare for a potential coast-wide strike in October 2024.

Looking at 2024, Descartes will monitor factors such as monthly TEU volumes that continue to surpass 2019 numbers, port transit wait times, the ongoing impact of the pandemic, the health of the U.S. economy, Panama Canal-based trade flow, Middle East conflict, and ILA/USMX contract negotiation to assess global supply chain performance. These factors have the potential to stress ports, affect global supply chain efficiencies, and disrupt trade flow.

The U.S. Court of International Trade has ordered U.S. Customs and Border Protection to begin unwinding tariffs imposed under the International Emergency Economic Powers Act (IEEPA), directing the agency to...

The Supreme Court’s decision striking down sweeping tariffs imposed under emergency powers may provide a temporary lift to U.S. port volumes—but the bump could fade quickly as trade policy uncertainty...

The U.S. Supreme Court delivered a landmark 6-3 ruling on Friday striking down President Donald Trump’s sweeping tariffs imposed under the International Emergency Economic Powers Act (IEEPA), setting off a...

February 20, 2026

Total Views: 1351

Get The Industry’s Go-To News

Subscribe to gCaptain Daily and stay informed with the latest global maritime and offshore news

— just like 107,412 professionals

Secure Your Spot

on the gCaptain Crew

Stay informed with the latest maritime and offshore news, delivered daily straight to your inbox

— trusted by our 107,412 members

Your Gateway to the Maritime World!

Essential news coupled with the finest maritime content sourced from across the globe.

Join The Club

Join The Club