By Mike Wackett (The Loadstar) –

The Red Sea crisis, driving extended voyage times around Africa, is creating simulated cargo demand and masking the growing imbalance of supply versus demand in the container liner industry.

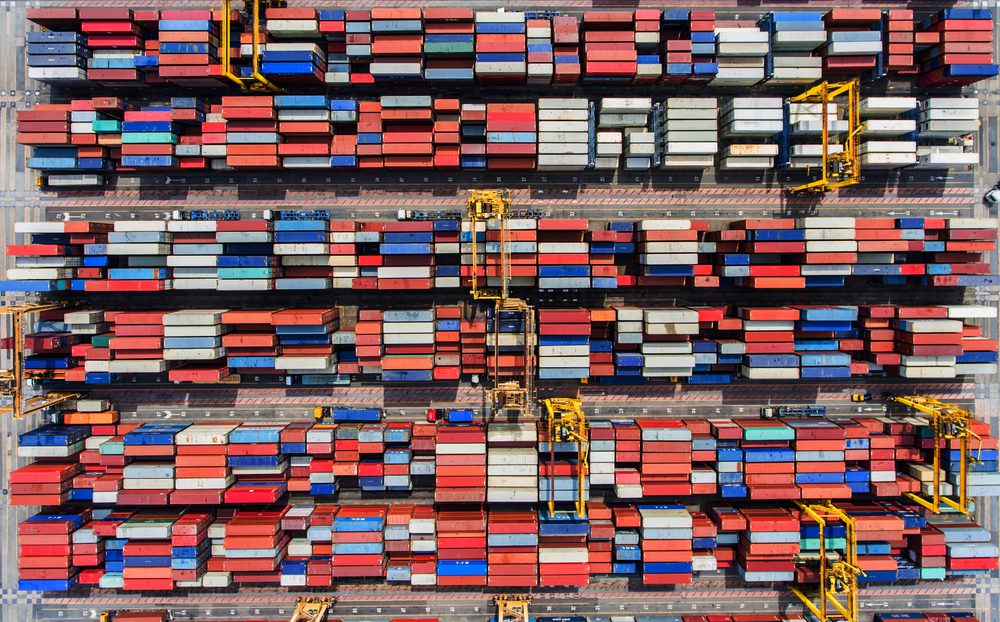

According to Alphaliner data, some 350 newbuild container vessels, equalling a massive 2.3m teu of capacity, were delivered last year, representing an 8% increase in cellular global capacity, set against anaemic growth.

Moreover, an analysis by Bimco reports that there are 478 more, with some 3.1m teu of capacity, scheduled to hit the water this year, which would potentially add a further 10% to the global fleet.

And Bimco said these newbuilds would also be heavily concentrated on the larger sizes.

“Another 83 ships larger than 15,000 teu are expected to be delivered in 2024, adding 1.4m teu to the segment’s capacity and doubling its capacity in just four years,” said Bimco.

In contrast, the shipping association said it expected growth in container trades to be “significantly slower”, increasing demand for ship capacity by a modest 3% to 4% this year.

At the other end of the spectrum, container vessel demolition sales are expected to continue their recovery.

Alphaliner reported a slight “bounce-back” in the sector in 2023, with 87 vessels, for 167,000 teu, sent for recycling.

This followed two years of virtually no activity in demolition sales, as carriers and non-operating shipowners held onto their assets due to strong demand and daily hire rates often substantially in excess of vessel operating costs.

Nonetheless, the consultant said, vessel deletions last year had fallen “well below expectations” and were “insufficient to address the rising overcapacity the shipping industry is facing”.

But Alphaliner is more bullish on vessel scrapping for this year, predicting that about 375,000 teu of capacity could be recycled – the highest figure since 2017, when demolition sales reached 414,000 teu.

“With just under 3m teu of tonnage aged 20 years and above, there is an obvious reservoir of scrap-able ships, even if many vessels in this age group are expected to continue to trade in the foreseeable future, especially carriers’ ships,” said Alphaliner.

However, it said competition from energy-efficient modern tonnage and a slump in charter rates, due to weak demand and overcapacity, could ultimately convince owners to scrap their elderly tonnage.

But while the disruption in the Red Sea continues, idled ships are being reactivated, sub-let offers are being taken off the open charter market and newbuild ships are being deployed immediately upon delivery.

“Diversions via the much longer Cape of Good Hope route create an artificial cargo demand that cargo volumes alone would not have supported,” said Alphaliner. “The uncertain near-term outlook on the Red Sea situation and the traditional rush to get cargo shipped out before the Chinese New Year holidays, will likely induce extra demand for shipping capacity in the coming weeks.”

It follows that Alphaliner’s commercially idle vessel capacity survey declined as of 1 January, to 106 ships for a total of 289,437 teu, representing 1% of the total global fleet.

The Loadstar is known at the highest levels of logistics and supply chain management as one of the best sources of influential analysis and commentary.

Editorial Standards · Corrections · About gCaptain

Join The Club

Join The Club