Teekay reported their FY 2012 financials today and if there was one word to describe Teekay operations at this very moment, it would be “Growth.”

“The improvement in our fiscal 2012 results compared to the prior year largely reflects the profitable growth from our continued investment in our fixed-rate gas and offshore businesses as well as our cost reduction initiatives,” commented Peter Evensen, Teekay Corporation’s President and Chief Executive Officer.

Teekay reports their Q4 2012 total cash flow from vessel operations was $217.9 million, up slightly from the same period of the prior year. For FY 2012, they experienced an adjusted net loss of $54.9 million, or $0.79 per share, in contrast to losses of over $100 million in 2011, and $120 million in 2010.

“Our fiscal 2012 results include a full year of cash flows from the two FPSO units acquired from Sevan at the end of 2011, cash flows from the LNG/LPG and shuttle tanker newbuildings that delivered during 2011 and early 2012, and cash flows from our 52 percent interest in the six LNG carriers we acquired from A.P. Moller-Maersk in the first quarter of 2012.

In addition, cash flows from our existing assets increased during 2012 due to the renewal of offshore and LNG contracts at higher rates, reduced operating expenses in our conventional and shuttle tanker businesses resulting from an organization realignment, and lower time-charter hire expenses due to the re-delivery of several time-chartered in conventional tankers, partially offset by the Petrojarl Banff FPSO being off-hire since its storm-related incident in December 2011.”

Had the Petrojarl Banff FPSO not sustained storm damage, Vincent Lok, Teekay’s Chief Financial Officer noted in a conference call, “full year net losses would have been closer to $19 million.”

“Bumping along the bottom”

Mr. Evensen notes that the negative outlook for 2013 within the conventional tanker market will likely continue due to “weak spot tanker rates, delays to the expected tanker market recovery, and further reductions in conventional tanker values during 2012.”

Teekay predicts that Aframax fleet growth in the coming years will be flat, as opposed to slight, single-digit growth of the global Suezmax and VLCC fleets.

Much of Teekay Tankers’ tonnage had been fixed on longer term contracts over the past few years, “which was a good move,” says Evensen, but as the industry appears to be “bumping along the bottom, we are looking at an interesting time to acquire assets right now.”

On the offshore front, Teekay announced that the Cidade de Itajai FPSO unit, which is jointly owned and operated by Teekay and Odebrecht Oil & Gas through a 50/50 joint venture, achieved first oil last week on its Brazilian offshore field and has commenced operations under its nine-year time-charter contract with Petrobras.

The FPSO unit, which was recently converted from an Aframax hull at Sembcorp Marine’s Jurong Shipyard in Singapore, is designed to process 80,000 barrels of oil per day and compress two million cubic meters of natural gas per day.

The Cidade de Itajai is the third FPSO unit introduced into the Brazil offshore market by the Teekay group. This includes two other FPSO units owned by Teekay’s publicly traded subsidiary, Teekay Offshore Partners L.P., the Cidade de Rio das Ostras FPSO and the Piranema Spirit FPSO.

Teekay notes that the financing is in place for a 50% ownership transfer of the Cidade de Itajai in the next 30 days to Teekay Offshore Partners.

The Voyageur Spirit FPSO was installed in September 2012 at the Huntington Field in the UK sector of the North Sea, image courtesy Sevan Marine

Teekay notes the field installation for the Voyageur Spirit FPSO continues to progress, with the unit expected to achieve first oil in March 2013.

Construction of the Petrojarl Knarr FPSO continues at Samsung Heavy Industries with and expected delivery in the first half of 2014. In December 2012, BG Group, exercised its option to extend the firm period of the Petrojarl Knarr time-charter to 10 years.

Upon delivery, it will commence operations on the Knarr field, offshore Floro, Norway’s westernmost town. The Knarr field is estimated to contain recoverable reserves of some 60 million barrels of oil equivalents.

Teekay notes that they expect rough average EBITDA of around 130-140 million per year and that now the long term charter is in place, the can now move ahead with debt financing options.

Construction is also proceeding on schedule on all four of Teekay Offshore’s shuttle tanker newbuildings, which will operate under 10-year time-charters with BG in Brazil upon their respective deliveries in April through November this year.

In addition, Teekay LNG Partners recently completed the acquisition of a 50 percent interest in a new LPG joint venture with Exmar and ordered two fuel-saving newbuilding LNG carriers, which are scheduled for delivery from DSME in the first half of 2016. Teekay notes that they expect to have long-term contracts in hand for the two vessels before shipyard delivery.

On the subject of their fixed yearly divided, Teekay notes that their mission at the moment is to “accumulate cash to invest in newbuildings or assets.” In their conference call they note that, “Traditionally, it’s been to issue equity, but we don’t feel that issuing equity at low share prices is the way to go.”

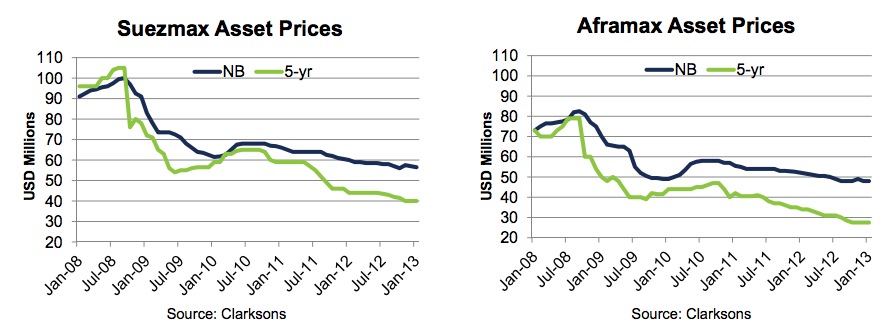

Teekay notes in their presentation a 20-25% decline in asset prices in 2011 with a further 15% in 2012, Click for larger

Throughout their call this morning, Teekay restated their goals for fleet growth and newbuilding, a firm exclamation to their view that the tanker market is headed for a recovery.

April 19 (Reuters) – A New York state agency on Friday said it had failed to reach final contract agreements with the developers of three major offshore wind projects, blaming a decision by General...

(Bloomberg) — The closure of one of the East Coast’s busiest ports after the collapse of Baltimore’s Francis Scott Key Bridge has so far not led to broad price increases,...

(Bloomberg) — An Iranian ship that’s been linked to Houthi attacks in the Red Sea is returning home, removing a prominent asset in the area as the Islamic Republic braces...

April 18, 2024

Total Views: 1193

Why Join the gCaptain Club?

Access exclusive insights, engage in vibrant discussions, and gain perspectives from our CEO.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

Join The Club

Join The Club