(Bloomberg Gadfly) — The past week in commodities markets has been like a trip through the looking glass.

Gold generally benefits from geopolitical shocks — say, the election as U.S. president of a man who favors Japan building nuclear weapons and muses about not supporting members of Nato in the event of a Russian invasion. Instead, it’s fallen almost 4 percent since Wednesday.

Or take base metals. More than half of the copper consumed in the U.S. is in consumer goods, industrial machinery, transport equipment or electronics — precisely the sectors likely to take a hit if President-elect Donald Trump’s policies result in a reduction of cheap imports from Asia. But the red metal is up about 8 percent over the same period.

Now another industry has entered bizarro world. Publicly traded shipping lines in China, Japan and Taiwan surged in Asia Monday, with Cosco Shipping Co. jumping as much as 10 percent and Yang Ming Marine Transport Corp. adding more than 7 percent. Those moves are in stark contrast to the more explicable 7.8 percent decline that Denmark’s AP Moller-Maersk A/S suffered after the election last week.

Cosco Shipping intraday gain: 10%

What possible good news could be out there for this struggling industry?

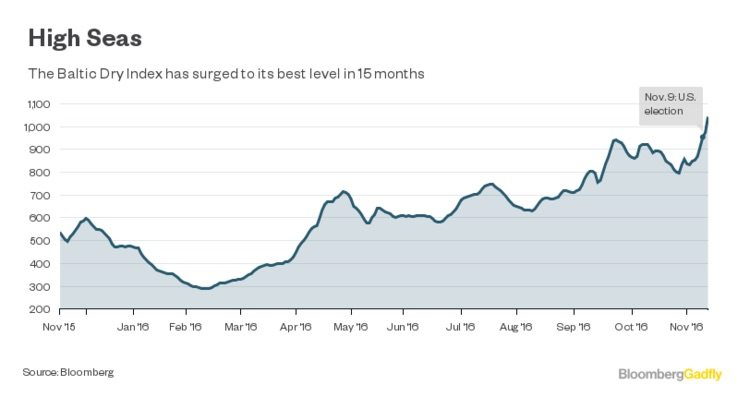

One theory is suggested by the Baltic Dry Index, a measure of the cost of transporting bulk commodities such as coal, iron ore and grains, which broke through 1,000 on Friday for the first time in 15 months. That’s great news for that segment of the shipping trade — and interestingly, it looks like a continuation of a trend that’s been underway for several weeks, so can’t be explained away as Trump Derangement Syndrome.

Perhaps the president-elect’s plans to set up a public-private fund to spend a trillion dollars on infrastructure is good news for shipowners? That’s the argument put forward by Central China Securities Co. to explain Monday’s share price action, but it doesn’t make a lot of sense. Construction tends to use a lot of heavy, cheap materials like steel and cement that aren’t so easily traded across borders — indeed, that’s probably one of the reasons that a protectionist politician is pushing such a plan.

Global trade volumes have been stagnating since a time when the idea of a Trump presidency was seen as a joke. They probably need some sort of active commitment at this point to reignite, and it’s hard to see how the past week’s events increase the odds of that.

It’s even harder to view the stock rally as a reaction to prices that had fallen too far. Valuations of major Asian shipping lines are at oddly high levels. All deservedly trade at a discount to book value, bar state-owned container specialist China Cosco Holdings Co. But measured against blended forward 12-month Ebitda, their enterprise values are through the roof. Of the three Japanese and two Chinese companies on the chart below, only bulks and tanker operator China Shipping Development Co. is below the aggregate EV/Ebitda of the S&P 500.

There may be one bargain half-hidden among the madness. The last time global trade flows dried up in 2009, China reacted by switching to a Trump-style domestic infrastructure boost, fueling booming demand for raw materials and driving up prices for iron ore, coal and hold space on the ships that transport them.

One of the commodity market’s main worries in recent months has been that Beijing’s latest episode of pump-priming may be coming to an end. But a more protectionist global economy is precisely the one in which such measures might be extended well into 2017. There are already signs that may be happening: State fixed-asset investment posted 18 percent growth on a three-month moving average basis in October, its fastest pace for that month since 2009, according to data released Monday.

That, and the favorable Baltic Dry, should draw a little attention on China Shipping Development. It’s a rare focused equity play on the global bulk commodities trade, which has most to gain from an Asian infrastructure splurge — and it’s on the lowest valuation of any of the shipping lines in the above chart. After all the confounding surprises of the past few weeks, even the idea of making money from investing in bulker ships doesn’t seem so strange.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

CAIRO, March 2 (Reuters) – The Houthi Transport Ministry in Yemen said on Saturday there had been a “glitch” in undersea communication cables in the Red Sea as a result of actions...

by Captain John Konrad (gCaptain) In the current American labor landscape, the stark contrast between the assertive strides of transportation unions and the maritime sector’s unique labor challenges is striking....

By Mikhail Flores MANILA, Dec 2 (Reuters) – Evacuations were under way in the Philippines after a quake of at least magnitude 7.5 struck the southern region of Mindanao on Saturday night,...

December 2, 2023

Total Views: 2164

Why Join the gCaptain Club?

Access exclusive insights, engage in vibrant discussions, and gain perspectives from our CEO.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

Join The Club

Join The Club

![A screengrab of a map showing an earthquake Mindanao, Philippines on Dec 2, 2023. (Image: US Geological Survey [USGS])](https://gcaptain.com/wp-content/uploads/2023/12/Screenshot-2023-12-02-at-10.45.17-AM-copy.png.webp)