As we all know, the current situation in the shipping world is that there is a large lack of demand against the current overall supply of container space. Today, the current fleet capacity is around 15.5 million TEUs. Since 2005, the total capacity has roughly doubled – literally.

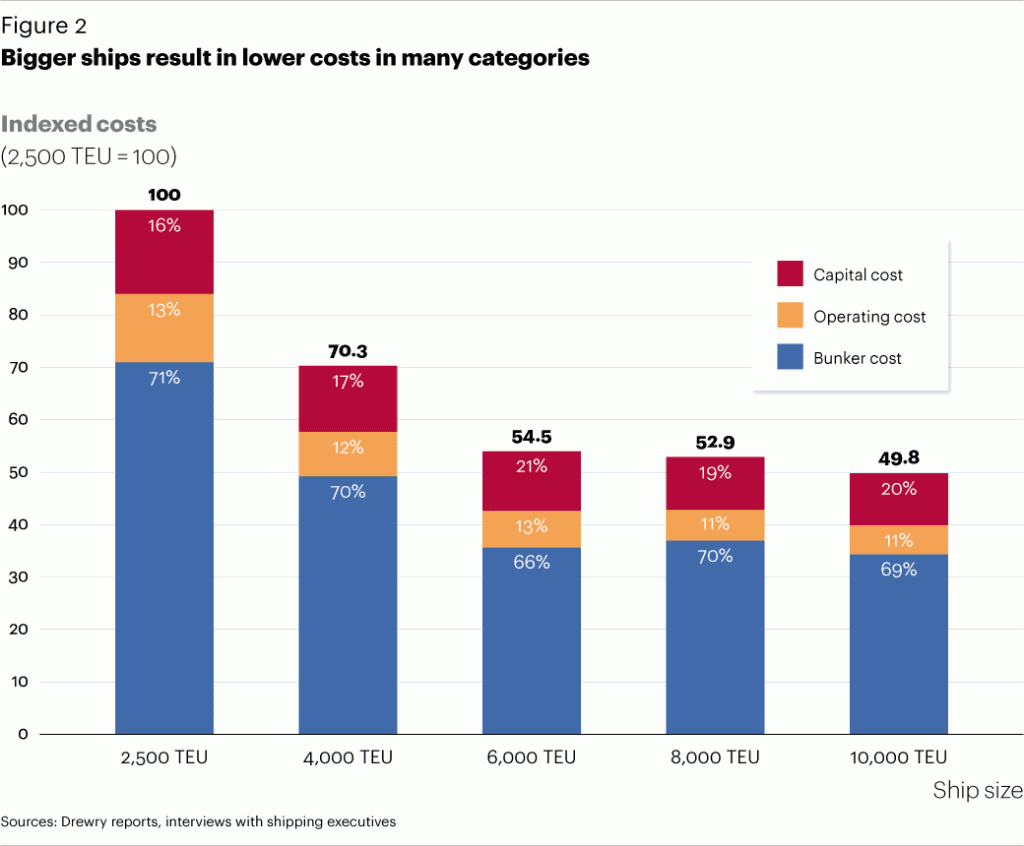

Because of the imbalance of supply/demand, carriers are losing blood and even declaring a negative balance sheet for end of 2012 (we are in May’12). This situation pushes them to the dilemma of getting bigger or getting smaller. Getting bigger means buying new, larger ships. These ships allow carriers to improve their cost effectiveness, work with smaller crews and lower their capital costs. On the other hand, some carriers are getting smaller; serving more niche markets where larger vessels will not call since that will reduce the efficiency of the vessel. You can imagine that a 15,000 TEU ship will not make 3 ports in the same country – if that country is not China.

These are the things we see and hear everyday. However a more important game is being played behind the scenes which have a crucial effect on the industry as whole.

According to Bloomberg; DNB ASA, the world’s largest arranger of shipping loans, expects the shipping industry to have a funding gap of $100 billion by 2015, as European banks are reducing their support to maritime transport. Even if US and Asian banks have an increased interest on maritime loans; EU banks account for 90% of the global ship lending. Considering net shipping loan losses at Nordea Bank AB (NDA), the world’s No. 4 shipping lender, tripled to 135 million euros ($179 million) last year because of “weak market conditions” and “a general decline in vessel values,”; everyone will be thinking twice before granting a loan. In addition to that, since there will be less vessel orders with reduced prices, it will be forcing some yards to close in the following 12 to 18 months.

How is this going to affect exporters/importers?

That’s our major question of course. Considering several factors; the EU Crisis, US getting out of recession, Arab spring is over; it will take another couple of years to get on track for sure. According to HSBC Global Connections, despite the current climate, the overall trend for international trade is positive with growth acceleration sooner than expected from 2014, than 2015. Over the next 5 years an annualized growth rate of %3.78 is forecasted for international trade. The main countries that will be carrying the growth are China and India, and China is expected to have an annualized growth of 6.60% in imports and 6.61% on exports; while India is expected to have 6.81% growth in imports and 7.60% in their exports from 2012 to 2016.

Now, according to 2010 stats, worldwide container traffic reached 560 million TEUs – an all-time high. China & Hong Kong Ports handle close to 169 milllion TEUs, 18% of this traffic. We need to keep in mind though, this is not only China exports/imports but also transshipped cargo that goes via those ports to other Asian nations.

With that in mind, if we take the growth rate with an average 6% for that region and multiply this with 169 million, we come up with a possible increase of 30 million TEUs annually and 500,000 TEUs weekly basis increase only in the region that handles 18% of global trade.

Now, lets go back to the supply side. The major banks will be reducing loans, there will be less ship orders and there will be less ship yards to build new ships. How is this going to affect the years 2014-15 and later?

I believe very tough years will come for exporters/importers in the sense of shipping costs and finding available space. We will see more of the complaints from US Exporters for not being able to find space and getting asked to pay very high freight charges like we were seeing in 2010. However, this time the difference will be, there won’t be any idle vessels sitting in Singapore or any new ordered vessels to come in and let everyone breath.

Considering today, this sounds improbable… Well, I believe the facts are out there and they show that the roller coaster ride we are on will just get crazier.

Can Fidan is originally from Turkey, where he got a Bachelors Degree in Economics at Koc University in Istanbul. After working 5 years at MTS Turkey he moved to Hong Kong as an MTS Representative where he stayed 2 years working on Asia Development of the group. After Hong Kong he came to MTS New York. He is currently the Vice President of Business Development and Export Manager at MTS Logistics, Inc.

COPENHAGEN, April 15 (Reuters) – Shipping company Maersk has not made any deployment changes after a Portuguese-flagged container ship was seized by Iran in the Strait of Hormuz on Saturday, the Danish company said on Monday. “We find recent...

WASHINGTON, April 15 (Reuters) – The FBI has opened a federal criminal investigation into the deadly collapse of a Baltimore bridge last month when a ship crashed into one of its supports,...

By Daryna Krasnolutska (Bloomberg) Russia and Ukraine may have struggled to shift things significantly on the battlefield for more than 16 months, but a new phase of the war is moving...

April 14, 2024

Total Views: 2084

Why Join the gCaptain Club?

Access exclusive insights, engage in vibrant discussions, and gain perspectives from our CEO.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

Join The Club

Join The Club